Are people who earn decent salaries too privileged to be thrown a bone by the government? Jenée Tibshraeny thinks not.

This story first appeared on interest.co.nz.

I would like to thank Housing Minister Phil Twyford for validating my generation’s “Ponsonby problems” as real ones. By setting the income caps for KiwiBuild eligibility at $120,000 for a single person and $180,000 for a couple, he is recognising the difficulties otherwise privileged young people face getting into their first homes.

But how dare we avocado-eating Auckland “yo pros”, who want everything now, make even the slightest whimper in the face of increasing homelessness and poverty? That’s true. We are fortunate in the scheme of things. We have good jobs, can afford to pay rent and the odd big expense that comes our way, and have a decent standard of living. Our “privileged people’s problems” are legitimate and essentially highlight just how tough things are for those who are less privileged. The most vulnerable should be the government’s main priority. Now that we have a new government, I feel like they are.

But in addition, it’s vital the government looks out for a generation ridden with student debt and locked out of the housing market. A business person recently told me my generation hadn’t done anything ground-breaking for society. Ouch. But are we really going to take financial risks to pursue our big ideas at age 30 when we’re still flatting and paying off our student loans?

The finances of the fortunate

According to Statistics NZ’s latest figures, the median student loan of someone who graduates with a bachelor’s degree or graduate diploma/certificate is $31,310. The median time it would take them to repay this loan is 9.4 years. The median loan size for someone who graduates with a post-graduate qualification (honours, masters, doctorate) is $35,310. The median repayment time is 7.9 years. Five years after study, the median earnings of a bachelor’s degree holder is 1.39 times that of New Zealand’s median income earner, while the earnings of a master’s degree holder is 1.6 times more.

Accordingly, the median bachelor’s degree holder earns $69,317 a year (gross) five years into their career, while the median master’s degree holder earns $79,789.

Let’s dig into the finances of the person with a master’s degree.

Gross salary per annum: $79,789

Less tax: -$17,250

Less student loan repayments: -$7,241

Less KiwiSaver contributions at 3%: -$2,394Less rent, power, internet, etc ($280/wk): -$14,560

Less food ($100/wk): -$5,200

Less transport ($40/wk): -$2,080= $31,064 per year, $597 per week

Less other expenses/spending money, the master’s degree holder might save about $18,000 a year, give or take. Remember, this is five years into their career – they would’ve saved less earlier on.

With a KiwiBuild home costing $600,000, even this “privileged” person would have to spend several years solidly saving and be willing to withdraw all their KiwiSaver to afford a deposit. Importantly, they would also have to be able to convince a bank they could service a mortgage.

If they made a 20% deposit and took out a 30-year mortgage at an interest rate of 4.5% pa, their weekly repayments would be $631 (according to interest.co.nz’s mortgage calculator). This would be teetering on unaffordable. Combining a second income would be a game-changer.

But ultimately, it would take a master’s degree, having a smooth path from school to university to employment, finding a well-paid partner, not forking out for a wedding, baby, travel, support for a struggling family member, etc, to afford a lower quartile home in Auckland by around 30.

There are a lot of ducks that need lining up.

Bigger trends support case study

House price growth really has dwarfed wage growth to the point even the most privileged young people – supposedly New Zealand’s future movers and shakers – are struggling to put down roots. Sure, many value other things and are choosing not to. Others are settling in cheaper parts of the country.

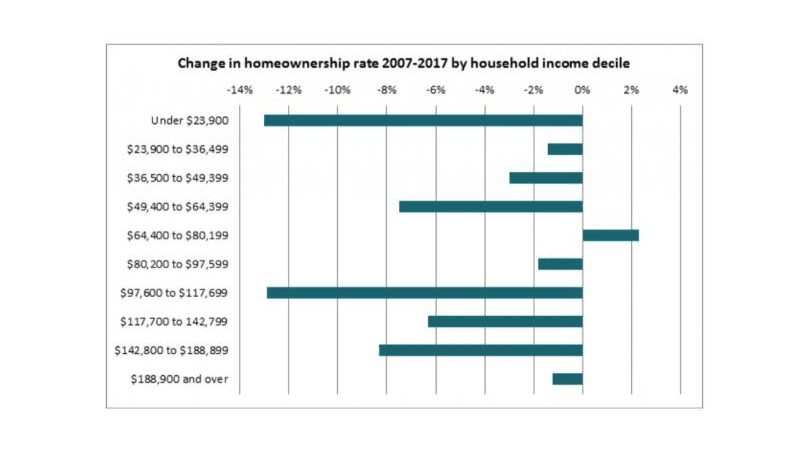

But it’s significant that only a quarter of adults under 40 own their own home, compared to half in 1991. Along with households that earn less than $23,900 a year, those that earn between $97,600 and $117,699 a year experienced the biggest drops in home ownership between 2007 and 2017.

Finding ideal solutions in an un-ideal world

So, are people whg earn decent salaries too privileged to be thrown a bone by the Government? Simply by being given a chance to put their name in a ballot to buy a modest home for $600,000? I don’t think so, provided the government sticks to its commitments and also invests more in state houses, Working for Families and the Families Package, for example.

The issue is, of course, that above average income earners – particularly those who are single – will still struggle to service a mortgage for a $600,000 house. While 92% of first home buyers will meet KiwiBuild’s eligibility criteria, a smaller portion will meet banks’ lending criteria.

This is not a failure of the KiwiBuild scheme, but one of the housing market and of the previous government that let it get to where it is. Until the building of lower cost homes ramps right up and supply of KiwiBuild homes meets demand, we will hear stories of young teacher couples on combined incomes of $120,000 missing out on KiwiBuild homes to engineer couples on $180,000.

This is unfair, but these situations should become less prevalent over time. Once building is well underway, it’s essential the KiwiBuild eligibility criteria is broad enough to prevent the government being stuck with an oversupply of low-cost homes.

KiwiBuild eligibility: one piece of a bigger picture

Yes, I am assuming the government’s ambitious goal of building 100,000 homes over 10 years will actually be achieved. This is crucial in ensuring house price growth peters right off, and that house price to income ratio starts looking healthier. It’s also crucial in ensuring KiwiBuild houses remain affordable, and the market isn’t such that buyers can flog them off after living in them for the minimum period of three years, only to pocket hefty capital gains.

Given the government isn’t doing anything to restrict capital gains earned on the sale of KiwiBuild homes, or requiring KiwiBuild homeowners to live in their homes for say five years, it’s clearly pretty confident it’ll be able to fix the housing market. While upping supply, restricting foreign ownership, extending the bright-line test etc are key, so is tweaking the broader tax incentives that make property investment more attractive than other types of investments. Hopefully, public sentiment shifts so that the Tax Working Group can present real fixes that may in the past have been politically unpalatable.

Coming back to the KiwiBuild eligibility criteria – the success of it will hinge on the success of efforts to fix housing market fundamentals and ensure the needs of our most vulnerable are met.

It’s from this base that a boost to the “privileged” young will be fair and effective.

This story first appeared on interest.co.nz.