The FMA’s annual sense check of KiwiSaver shows New Zealanders continue to embrace the scheme but the fees they’re being charged may not be doing them any favours.

Who is the Financial Markets Authority (FMA) and what’s this report?

The FMA is the government gatekeeper for our financial markets, and it is one of several bodies that oversee KiwiSaver. It puts out an annual report on the state of the scheme, and operates the KiwiSaver Tracker tool which lets you see how your fund is performing in relation to the fees it charges.

Is KiwiSaver going well?

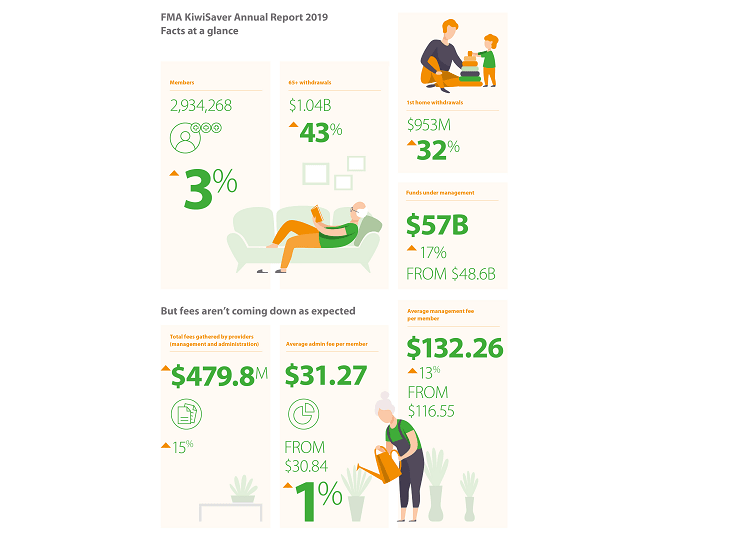

Yes, broadly. There are now 2.9 million KiwiSavers, and the number of people signing up to the scheme is steadily growing with 134,600 new members joining in the last 12 months, around the same number as the previous year.

The average member’s balance is now nearly $20,000 and KiwiSaver funds collectively manage $57 billion, up $8.4b on last year. A healthy $3.8b of that increase came from investment returns – 19% more than the previous year – and the KiwiSaver funds did well to achieve that given the turbulence on global finance markets at the end of 2018.

KiwiSavers are also starting to retire, and the amount of money withdrawn by people over 65 topped $1b for the first time. Meanwhile 39,600 members made the most of the scheme by withdrawing $953m to buy their first home, up 32% on the year before.

So are we all getting in behind KiwiSaver?

Er, not exactly. People might be signed up but it doesn’t mean they’re contributing. Two out of five members put nothing at all in last year, roughly the same proportion as the previous year.

And are there are a few bugbears with the scheme?

There most certainly are, the two main ones being the number of people sitting in default funds, and the amount of fees KiwiSaver providers are charging. More on these below.

Are there a lot of people in default funds?

Yes, and it was never the idea that they should all stay there. Default funds are supposed to be a first step when people enter the scheme and then they’re meant to choose a fund that’s right for them. Last year 52,000 people made an active decision to get out of a default fund, up from 28,000 the year before, and the nine default funds’ share of membership has continued to fall. But still more than one in 10 people are languishing in these low return funds.

FMA director of regulation Liam Mason say default funds might be all right for some people, but for a lot of others it means they’re missing out on valuable savings. Next year KiwiSaver statements will include a projection of what members’ balance will be on retirement. “I think that’s going to make it a lot more real for people.”

So why are they still in these funds?

The report shows that 20,000 people last year made an active decision to stay in their default fund, and that’s a big jump from the previous year. KiwiSaver providers say the reasons for that range from concern about market volatility to wanting to use the money for a first home deposit, and a perception that it’s the ‘best’ option. The providers also say members who’ve been in a default fund for a long time are harder to contact.

The term for the current default providers expires in June 2021, and government regulators are reviewing the setup.

What’s the issue with fees?

KiwiSaver providers charged $480 million in fees last year, up nearly 15% on last year. The FMA is grumpy about this, saying as the funds grew it had expected economies of scale to be passed onto members. But it’s not happening, and it will be asking KiwiSaver providers to ‘please explain’. Its KiwiSaver Tracker tool is still showing no clear link between higher fees and higher returns, apart from a couple of standout funds. The regulator has also done some research and found that KiwiSaver fees are high in comparison to similar funds in the UK.

The FMA’s Mason says the UK comparison shows the regulator needs to keep investigating, and it fits in with the work it’s doing with the banks and other financial institutions. “We want to challenge KiwiSaver providers to demonstrate value for money,” he says.