Nearly a quarter of a million of mostly young New Zealanders are now regularly dabbling in cryptocurrencies, which many professional investors see as little better than a scam. Are the crypto fans about to get burnt big time?

It’s a cheap shot that has an uncomfortable sneer to it: “You can’t live in a bitcoin!”

It’s a rejoinder I’ve heard murmured by a few of my boomer mates who can’t understand why so many of their Gen X/Y/Z staff members are actively trading and buying cryptocurrencies such as bitcoin and ethereum. But it’s a comment that’s often made out of hearing distance of this new generation of what used to be called ‘Mum and Dad’ investors. They feel it’s a true and clever thing to say, but they also know it carries more than a hint of smug entitlement that could get them into trouble with colleagues who buy bitcoin because they can’t afford a house.

That lack of affordability may even be the reason these well-paid renters have bought bitcoin in the first place – they’re hoping another spectacular jump in the value of the crypto-of-the-day gives them enough to buy a house, or least to put down a deposit deemed enough by the Reserve Bank to take out a home loan.

The implication of course is that these youngsters are crazy and should just do the sensible thing and buy an investment they can live in, like the house (and a few rentals) the older ones have bought over the years. But for many that has been a dream that faded through the last decade and was destroyed completely with the last 30% jump in house prices since the onset of Covid.

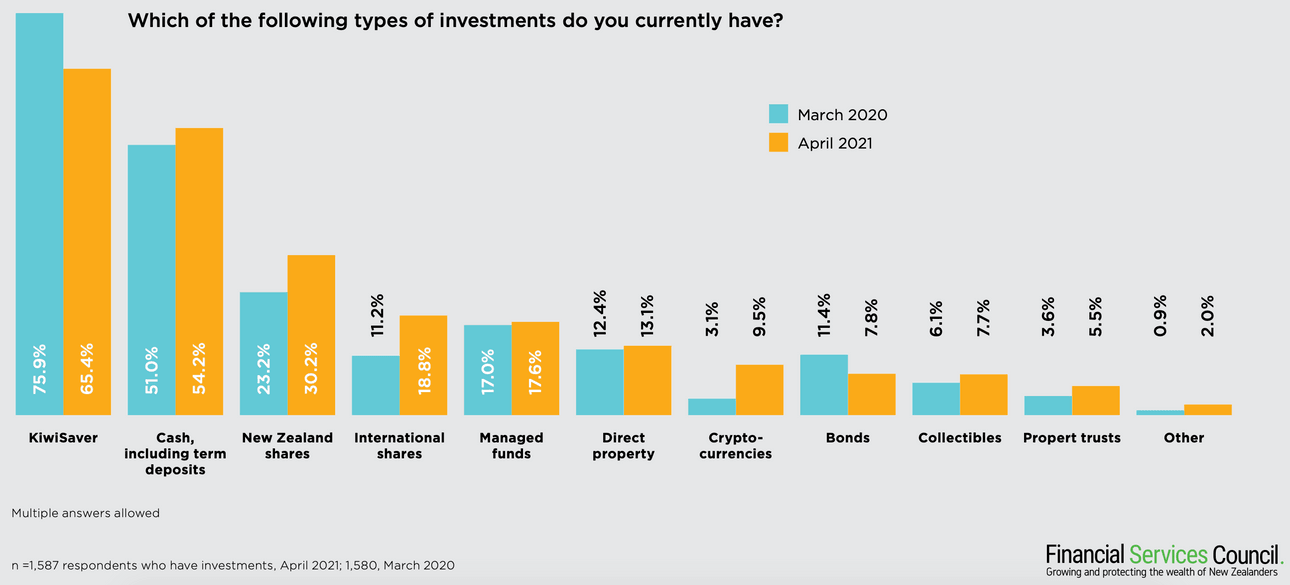

When going to open homes and auctions seems pointless, at least there is Sharesies and Hatch and InvestNow and Stake to trade on. And now there’s also a dozens of exchanges to invest in bits of bitcoin and ethereum and over 150 other cryptocurrencies. The best estimates are that around 220,000 New Zealanders (7.5% of the adult population) have traded or held some form of cryptocurrency over the last couple of years in more than 436,000 different accounts.

EasyCrypto co-founder and CEO Janine Grainger is right at the centre of the explosion in cryptocurrency trading and experimentation in New Zealand. EasyCrypto describes itself as a retail cryptocurrency platform that has handled over $1.1b worth of transactions since its founding by Grainger and her brother Alan in 2018.

It is the most popular accredited exchange in New Zealand, used to buy cryptocurrencies by a whole new class of investor familiar with the “micro” investing platforms such as Sharesies, Hatch, InvestNow and Stake. These people are also using crypto for various investments, including lending it out for annual returns of 5 to 10% for regular borrowers, and higher for riskier ones.

“The traditional original way to get into cryptocurrency is buy and hold – or hodl (Hold On for Dear Life) as the industry calls it – and sit on them in the hope that they go up in value,” Grainger tells me.

“And for people with currencies such as bitcoin that’s done very well over the long run. There’s also more and more different types of investments coming out now, with things like ‘staking’ where you can have assets that are not only exposed to potential changes in the value of the asset, but you’re also getting a return on the asset,” she says.

“Then another type of thing that we’ve started to see more recently is NFTs — non fungible tokens — basically think of them like digital collectibles.”

EasyCrypto is on quite the growth trajectory. Grainger has just wrapped up a $17m Series A fund raising round that brought in Nuance Connected Capital, along with Pathfinder, Icehouse Ventures, Even Capital, Indonesia’s GDP Venture and US firms Hutt Capital and Seven Peaks Ventures. It has grown to well over 60 staff and is rapidly hiring more.

It’s not just crypto. The demand for DIY investing is rampant and the scale in New Zealand terms is substantial. There are now over 355,000 people with Sharesies accounts, up more than 60% since before Covid. Another 110,000 have Hatch accounts and 40,000 are with Stake.

It wasn’t always that way. As recently as a decade ago, there were fewer than 50,000 ‘Mum and Dad’ investors who regularly traded shares through traditional brokers or through the online trading platforms of the big banks. Typically, they were older, and owned shares in locally listed companies with the aim of receiving regular and relatively large cash dividends.

These ‘Mums and Dads’ were often wary of enthusiastic claims or anything that looked too good to be true. They remembered the irrational exuberance of the mid 1980s when the dramas on stock markets made the evening news and entrepreneurs such as Bob Jones, Allan Hawkins, Bruce Judge, Colin Reynolds, Michael Fay and Ron Brierley were household names. Then came the 1987 stock market crash, which hit New Zealand individual investors harder than in any other market in the world. Companies such as EquityCorp, Ariadne and Chase Corp exploded into massive conglomerates of unrelated businesses held together by debt and byzantine corporate structures that evaporated as soon as the easy lending stopped.

A whole generation of share club enthusiasts who had mortgaged their houses to buy shares were wiped out and pledged never to go back into a market deemed closer to the wild west than anything fair or predictable. For 20 years, anyone with savings put it in the bank.

By the early 2000s, a few tens of thousands of investors had summoned up the courage to put their spare money into finance companies which, they had been reassured by advertisements in the newspapers, were as safe as the property they were secured by. Unfortunately, much of that security was on development projects, holes in the ground being dug by related companies in control of those same finance companies. A whole new slab of collapses among the likes of Bridgecorp and Hanover Finance wiped out confidence for a whole new generation of investor.

It has taken a couple of decades to iron the dodginess out of New Zealand’s share markets and then wipe away the memories and the dregs of the finance companies. The birth of KiwiSaver funds in 2003 has been a safe and well-regulated introduction for a whole new generation of investors — a type of gateway drug to stocks and shares.

Then the arrival of first Sharesies and then Hatch made it much easier to invest and cheaply trade small amounts in familiar listed companies and exchange-traded mutual funds (ETFs). Covid lit the touch paper for a whole new swathe of young investors with some time on their hands and access to tools that felt more like video games than boring old stock market investing.

The investment explosion since mid 2020 has taken many by surprise and raised concerns that a new inexperienced generation may be putting their money into risky places such as cryptocurrencies. Plenty of bankers and big-time fund managers have judged cryptocurrencies a giant scam that will explode in everyone’s faces as soon as the money printing stops.

But that hasn’t happened. Yet. And many crypto holders are confident this time is different, if only because investors are much more diversified.

Grainger thinks New Zealanders have invested in and traded around $2b in cryptocurrencies in the past year, but that still pales in comparison with the $81b in KiwiSaver funds, the $58b in the NZ Super Fund and the $120b managed by other New Zealand-based funds. Most of that is spread far and wide in bonds, stocks, property and other assets that tend not to move up and down all at once.

The regulators are also keeping a close eye on the development of the sector.

“The FMA has guidance out recently talking about investing in crypto assets and the recommendations for New Zealanders was if you’re going to go get involved, use a New Zealand provider that is regulated and registered here in New Zealand,” she says.

“The New Zealand providers have registered as financial service providers. That means they’re part of a dispute resolution scheme – if something goes wrong, you’ve got a really clear avenue to go down to get that dispute sorted.

“They’ve also got all the right AML (anti-money-laundering) controls in place and that should give you confidence that you’re engaging with parties who are trustworthy and not fly by nighters.”

Diversification is a sensible recommendation for any investor and investment type, she says.

“I would encourage people to look at how they diversify their portfolio, because – [this is] not financial advice, and definitely not individual advice – but as a general rule, diversification is really important,” she says.

“You don’t want all your eggs in one basket. And I see cryptocurrency as one of the buckets that you should be considering as part of a diversified portfolio. It can be a higher-risk bucket that can have higher rewards and maybe it’s 5 or 10% that you’d look at putting in, but it’s worth looking at putting some portion of your portfolio into those asset classes.”

Some are feeling friskier than others, though.

A survey done this year before the latest lockdowns of investors by the Financial Services Council found younger men were the keenest on cryptocurrencies, and the most confident of making big profits.

Not everything changes.

Follow When the Facts Change, Bernard Hickey’s essential weekly guide to the intersection of economics, politics and business on Apple Podcasts, Spotify or your favourite podcast provider.