New Zealand’s housing market is going ballistic, defying economic forecasts and historic trends. Michael Andrew asks the experts what’s causing the clamour and what it means long term.

Six months after Covid-19 first reached our shores, New Zealand’s economy has officially moved into recession. GDP is down 12.2% – the largest drop on record – spending activity has slumped, unemployment is rising, and our hospitality and tourism industries have been decimated by two lockdowns and a world slowed down to a sickly limp.

It’s a once-in-a-century tempest that is foundering almost every single ship in its path, and slowly making many of us poorer. And yet, in the midst of it all, perfectly robust and sailing along at a rate of knots, is New Zealand’s apparently unsinkable housing market – enjoying some record-breaking spikes.

Everyone seems to have a similar version of the story that goes something like this: a neighbour or friend recently listed a house for $1m, 80 couples came to the open home, and it sold for $1.2m cash a few days later.

The anecdotes are everywhere, but what does the data say? According to Reinz, last month’s median house price across New Zealand increased by 16.4% from the same time last year to $675,000 – up from $580,000 in August 2019 and up from $659,000 in July.

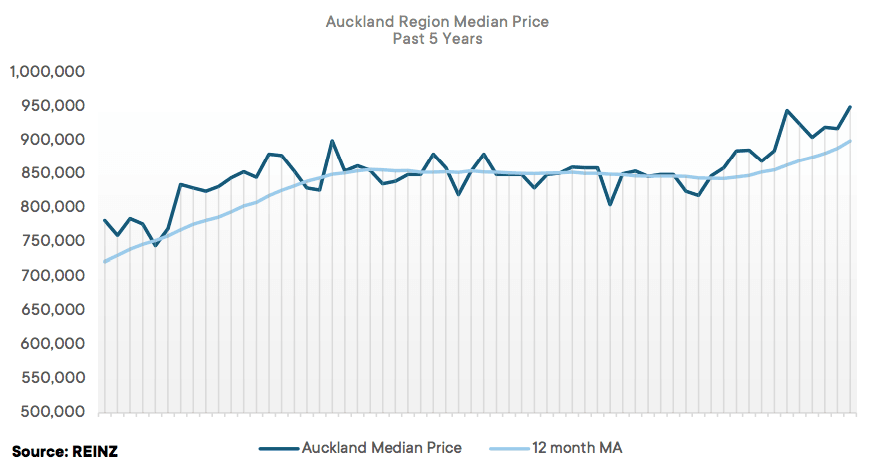

In Auckland, median house price increased by a record 16% to $950,000 from $819,000 at the same time last year, and up from $918,097 in July this year.

They’re startling stats that fly in the face of virtually every single other economic performance metric. Even the economists were forced to revise their forecasts, which initially predicted a heavy drop in prices.

“The housing market has proven incredibly resilient throughout the pandemic… and it’s surprised many,” said Kiwibank economist Mary Jo Vergara.

She called it an “atypical result” to emerge in such an economic crisis, which, because of the heightened uncertainty, was expected to hamper any appetite and ability to buy or invest in housing.

“Usually you’d see a drop in house prices somewhat equivalent to a rise in the unemployment rate, similar to what we saw during the GFC. Covid-19 is a completely different crisis. We’ve seen a lot of engagement from first-home buyers and investors especially. For those relatively sheltered from the crisis, who have secured employment, the market is theirs for the taking.”

So that’s the economists’ take. But what’s the reality on the ground? Other than the rumours, is the activity at the open homes and auction houses really as frantic as is being reported?

“It’s mental,” said Tim Hawes, of Ray White Kingsland in Auckland.

“Totally mental. The reports are true. People can’t find what they want or they keep missing out on things, and then they’re just like: ‘Screw it, money’s cheap, the LVRs have changed, my job’s OK, and we need something to live’.”

Hawes said he’s seeing extraordinary buyer behaviour that started in January and continued throughout the year, abating briefly during the two lockdowns. In one case, he said, a couple were looking for a house in Auckland’s Point Chevalier. After missing out multiple times, they found one with the asking price around $2.5m and paid $3m so it wouldn’t go to market.

“Stuff like that is happening, and it’s pure desperation. No one’s panic buying, they just want to bloody live somewhere and they’re sick of mucking about and they’re sick of missing out on stuff.”

Housing mania is not an unusual phenomenon in central Auckland, which typically exists in its own microcosm with prices far higher than the rest of New Zealand. However, the desperation has clearly spread beyond the city borders and into outlying suburbs and the regions. Terry Gray of Barfoot and Thompson Titirangi said houses in Piha and Karekare that have been on the market for over a year have all sold over their CVs in the past few months.

And according to Reinz, Gisborne’s houses have been selling on average 71% higher than their CVs, the highest in the country, followed by Southland’s houses at 43% beyond their CVs. Reinz chief executive Bindi Norwell said pent-up demand following the lockdown has contributed to the premium people are prepared to pay.

What’s causing it?

While pent-up demand is invariably a factor, New Zealand’s housing woes have long been complex, and there’s undoubtedly far more at play. New Zealanders returning from overseas have been cited as the reason for the heightened activity, and while they will certainly be influencing some of it, their arrival has been offset by the near total decline of other inward migration.

Although there’s no single reason why the market continues to stay buoyant in the current crisis, Hawes said two dominant factors are combining to exacerbate the demand: low interest rates and a terminal housing stock shortage.

People can now afford to borrow more and pay less on their regular mortgage repayments, making the prospect of home ownership more achievable. At the same time, they’re coming up against thousands of others in the same position and competing for a very limited number of homes, resulting in the excessive competition and bids Hawes is seeing in the field.

“The volume of people trying to buy just can’t be satisfied with what we have currently in terms of stock levels. We were historically down in stock anyway and then you just throw a lot of people in – that creates a bit of a critical mass.”

As for the low interest rates, economists and policy makers have been coming to grips with how truly effective they’ve been to bolster housing demand against slowing consumption activity and rising unemployment.

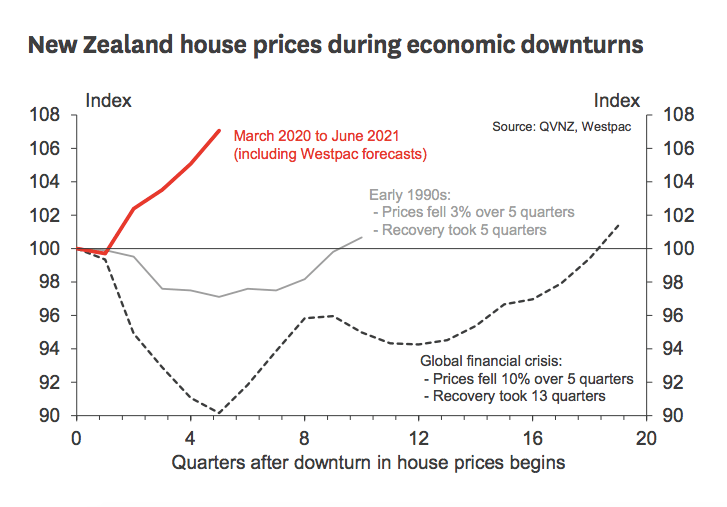

Westpac chief economist Dominick Stephens – who last week revised his forecast from a 7% drop in house prices to a 3% rise by December – says the market performance was surprising, but is now perfectly understandable considering the mechanisms at play.

“We now have the benefit of hindsight, and it tells us that low interest rates are playing an even more powerful role than anticipated, while rising unemployment is playing less of a role. Therefore the balance between the two forces is a bit different to what was anticipated, and has resulted in a small rise in prices. Live and learn.”

“Surely people will now accept the role that interest rates have played in the big increase in New Zealand house prices in recent decades.”

Are higher prices a good thing?

Dr Andrew Coleman, from the University of Otago’s department of economics, agrees that the low interest rates are having a tremendous effect on people’s appetite to borrow and spend – but not in the way it was intended. He says an inflated housing market is almost an unintended and disadvantageous by-product of the Reserve Bank’s aim to stimulate activity through the OCR.

“In an ideal world, low interest rates would be stimulating businesses to invest more; that would be, I suspect, the big hope of central banks to lead to higher investment activity.”

“It seems that the lower interest rates are leading to a big expansion in credit, which is facilitating asset exchange, rather than facilitating new activity.”

In other words, the Reserve Bank’s low interest rates have made people eager to buy or invest in houses at a premium – thereby pushing up prices – but have not motivated people to spend more at their local retail store or restaurant, or banks to loan to SMEs in order to expand.

But even if it isn’t the ideal outcome, isn’t stimulating the demand for housing a good way to drive economic activity? After all, the economic theory suggests that higher house prices make owners feel wealthier, therefore compelling them to spend more.

“I don’t think it’s a good thing at all,” says Coleman. “We’re pricing out a whole generation from residential real estate markets. We have extraordinarily high house prices at the moment, and I can’t see how we can be happy if lower interest rates – which are intended to stimulate activity – are creating even higher prices.”

“I mean, if we found that cars were twice the price in New Zealand than they were in other countries, we wouldn’t say ‘oh, that’s great for people who own second-hand cars,’ we would say, ‘there’s something wrong with the economy here that we can’t access cars at reasonable prices’.”

As the government pulls all the levers to stimulate activity and bring New Zealand out of recession, interest rates are expected to fall even lower in the coming years. However, they will inevitably start rising again. When they do, Coleman says homeowners will typically prioritise their higher mortgage payments and spend less, which will invariably hurt small businesses in the local economy.

“When interest rates rise, most of them do whatever is necessary to stay in the house and pay the mortgage. But it means that there’s a big curtailment of discretionary spending. You don’t go and buy takeaways as much for instance.”

“So it does have quite adverse economic effects. A lot of discretionary local businesses find that their lives become very tough.”

Of course, there might be several years between now and then. In the meantime it’s a case of watching the lower interest rates and housing shortage inflate the market like a balloon, levitating prices beyond the reach for many.

Kiwibank’s Mary Jo Vergara says that although the current run has meant the long-awaited “correction” in the housing market will not be as severe as expected, her team is still forecasting a 5% drop in prices as unemployment peaks over the coming years. However, the way the market is behaving is anyone’s guess, and she says another upward revision is certainly possible.

We will be much deeper into the recession when – and if – house prices finally start to come down. The question is, will many of us even be in a position to take advantage of it by the time that happens?