Rebecca Stevenson takes a look back at the tenure of ‘Mr Milk’, Theo Spierings, atop our biggest company.

It’s our biggest business (yet it’s a co-operative) and its chief executive Theo Spierings also earns the highest salary in New Zealand – a lottery dream of a wage packet of about $8.3 million a year, or $159,000 a WEEK, or $22,700 a DAY. What would you do?

It’s a huge amount of money, yes. But Fonterra is a massive operation, owned by an estimated 10,000 dairy farmers (often called farming families, but it’s tricky to discern how many farms are owned by corporations, and Fonterra can’t give a number). Fonterra is the largest exporter of dairy products in the world, collecting billions of litres of milk, with about 95% of that milk exported. It’s estimated to account for about 30% of the world’s dairy exports, so yup, Fonterra is kind of a big deal.

For the 2017 financial year Fonterra pulled in revenue of $19.2 billion and net profit after tax of $745 million. For the farmers who pull on the gumboots every day and supply Fonterra its milk, the last financial year brought a ‘Farmgate Milk Price’ of $6.12 per kilogram of milk solids, and each share in Fonterra paid out a dividend of 40 cents.

At the helm of this mammoth milk machine has been Dutch dairy executive Theo Spierings. But this week saw the man dubbed “Mr Milk” step down (later this year) after seven years at the top. Why now? It could just be a little matter of a $348m half-year loss in 2018. But first, let us take you through Spierings’ stint at Fonterra; year by year, record by record – but also scandal by scandal.

2011: the arrival

Spierings’ appointment was announced in July 2011 but really the previous CEO Andrew Ferrier was still in charge for most of the year.

Spierings arrived in a record year for the co-operative. Fonterra reported revenue of $19.9b, an after tax profit of $770m (pretty similar to 2017), and paid out to farmers milk payments and dividends totalling $10.6b – $2.4b more than in 2010 and $1.5b more than Fonterra’s previous best year in 2008. Tickety-boo!

Little did Spierings know it, but an event was impending that would set in motion a PR crisis forever denting fortress Fonterra’s aura of invincibility.

2012: a ticking bomb is set

February to be precise. At the company’s Hautapu plant in the Waikato a large dryer was being examined, and during that process a torch being used “came into contact with a part of the equipment, breaking the hard torch lens,” a report later commissioned by Fonterra found. These bits of broken plastic had a catastrophic impact, ultimately triggering a botulism scare after testing in March 2013 identified high clostridia levels in a finished product made for a Fonterra customer.

The bomb was set, and the timer was ticking. But consumers, and Fonterra HQ, were unaware anything was amiss, and its annual result was duly announced for the 2012 financial year with flat (but still massive) revenue at $19.8b, while net profit after tax was $624m on “record milk flows”.

Spierings had also started a drive for efficiencies, which continued throughout his reign. The company said in 2012 a “strategy refresh” would see it slash expenses by $90m, and a further $60m in 2013. The cost of the restructure? $30m.

In the same month as its annual result, however, Fonterra discovered traces of fertiliser aid dicyandiamide or DCD (it helps to stop nitrate leaching into waterways and wells) in its dairy products, but said nothing until the new year. Another bomb started ticking.

It also introduced its Milk for Schools programme in December, offering free milk to all school kids. Spierings closed out his first full year in charge on a high, when the Fonterra Shareholders Fund floated on the NZX after publishing a prospectus in October.

2013: the Botulism scare bomb explodes

In January the DCD issue hit the media and the Wall Street Journal posed the question “Is New Zealand milk safe to drink?”. Fonterra said it was, that the DCD was only at low levels.

In the background the botulism bomb was well and truly primed. In March products started testing positive for clostridium, but it was months until Fonterra made any moves. Finally, in August, it notified the eight customers who received the contaminated whey and on 3 August it went public.

People were pissed. They were pissed about the delay in Fonterra telling them about the potential contamination, they were pissed about what little they were told about the contamination (imagine you were feeding your baby infant formula at the time – the disease is dangerous and potentially fatal), they were pissed Fonterra didn’t know whether there was toxic infant formula, and the people that were already pissed that Fonterra even existed were pissed and were also busy saying ‘I TOLD YOU IT WAS TOO DAMN BIG’.

And what did Mr Milking Millions say? “The precautionary recall challenged the co-operative, but has also provided the opportunity to make a profound change for the better. Within days of locating and quarantining product, we began an operational review to find out what happened, why, and what we must do to prevent this from happening again – and we are now implementing the recommendations of the review.” No drama then.

In 2013 Fonterra recorded revenue of $18.6b (down 6% year on year), but net profit after tax of $736m. Farmgate Milk Price was $5.84, with a dividend per share of 32c, making a total cash payout of $6.16 per share for shareholders/farmers. Not too shabby. Considering.

2014: the record highs

Except the fake botulism scare was now going to poison Fonterra anyway, as its clients looked to recoup losses on the product they’d had to recall, not to mention the reputational damage of a global scandal.

The price of this toxic scare, infant formula maker Danone estimated, came to $1b. On 8 January, Danone filed a dispute notice against Fonterra in Singapore and legal action in New Zealand. Danone also stopped using Fonterra’s factory in Darnum, Australia, which analysts later said, eventually led to Fonterra’s deal with Chinese company Beingmate (Beingmate purchased about half of the factory from Fonterra).

In April it was fined $300,000 for the botulism scare but Fonterra shrugged off its woes, booking revenue of $22.3b for 2014, and a final cash payout of $8.50 a kg for shareholders on a milk price of $8.40 – and a more modest dividend of 10c because net profit after tax was only $179m.

Just before it announced its results, it also announced a partnership with Chinese baby food and formula maker Beingmate Baby and Child Food Co. The deal, Fonterra said, was collectively worth $1.2b, with Fonterra first buying an up to 20% slice of Beingmate for an estimated $615m. The deal, Spierings said, would be a “game changer”.

2015: the Beingmate deal

A series of job cuts started early in the year attracted negative publicity when it ramped up to encompass 500 jobs (to cut another $60m in costs) but in the end another 250 jobs would be lost before the year ended.

Spierings’ pay rose in 2015 a hefty 18% to almost $5m, which provoked outrage about excessive pay to the executive; in tandem with the job losses it was not a good look. Fonterra announced a net profit after tax of $506m for the financial year ended 31 July, up a whopping 183%, but revenue was down to $18.8b. The cash payout was $4.65 per share.

Spierings said the company had achieved the result by focusing on “cash and costs”. Fonterra’s Beingmate deal had closed, falling short of the 20% Fonterra had wanted, with the company paying about $755m in the end for about 18% of the Chinese company (analysts were already sounding the alarm about its new partner’s financial health).

It ended the year by introducing three-month payment terms to some of its suppliers; a move Spierings would later trumpet had saved the dairy giant about $50-$70m and one we are still talking (in not very complimentary terms) about now.

2016: volumes down; profit up

Fonterra introduced Disrupt, its internal innovation project which allows any Fonterra worker or team to pitch ideas which can then be executed. This project the company estimates, has added about $70m of new revenue.

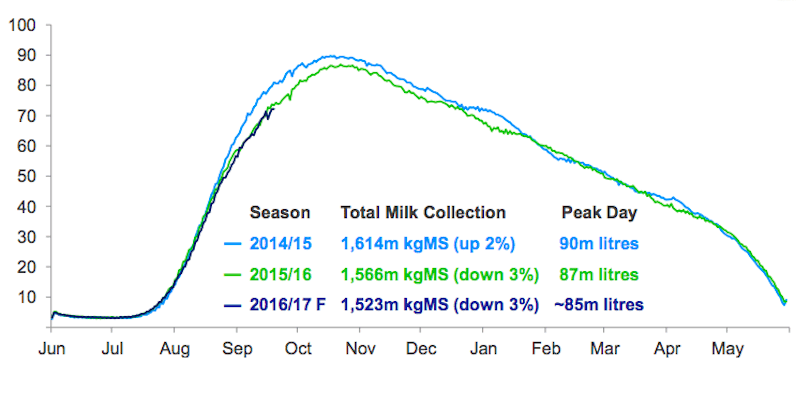

But the July 2016 financial year saw milk volumes decline for the second year in a row and revenue was down to $17.2b, but there was a 65% increase in that all important net profit after tax, to $834m. *Whistles*. Spiering pinpointed Fonterra’s ability to sell more milk at higher prices as the key underpinning the good after tax result, turning liquid milk into “higher value products”.

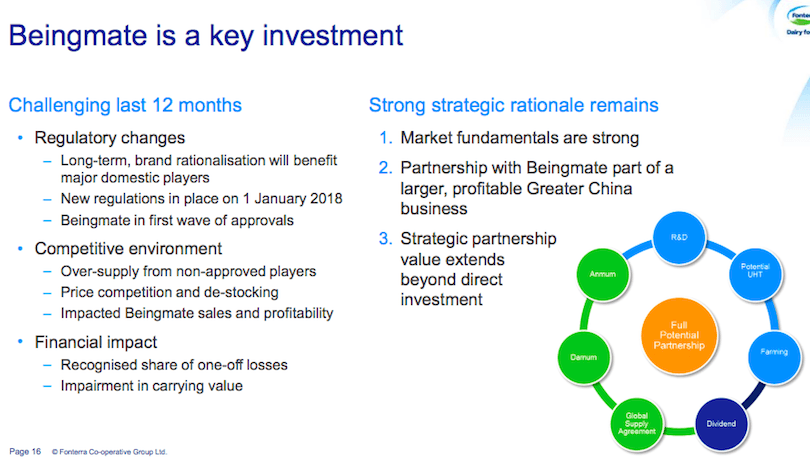

The Beingmate investment continued to unravel and in June the company forecasted a $48m loss after its own milk powder scandal and again, analysts at home warned worse was to come.

2017: counting the $183m cost

The year started with a bang of good publicity, Fonterra introducing the Fonterra Ventures team to seek out innovative ideas from outside the company – echoing its move to disrupt its business from the inside.

Milk supply levels recovered, and a positive global dairy outlook jollied our biggest company along, but both the Danone dispute and its investment in Beingmate overshadowed the general good vibes. Revenue (as stated above) had come back to 2011 levels.

Fonterra claimed things at Beingmate were fine, but in September analysts started screaming about the Beingmate deal. “In short, Beingmate has lost sales, missed FSF targets and likely lost reasonable market share in the last three years and FSF has been largely silent on it with investors,” a wealth manager said.

In December its arbitration with Danone over the 2012/13 botulism scare was settled, costing it $183m and its shareholder/farmers were understandably seething. Spierings was “disappointed the arbitration panel did not fully recognise the terms of our supply agreement with Danone, including the agreed limitations of liability”.

A bullish Spierings said Fonterra was in such financial health that it could meet the recall costs, and it must have been a relief to have a line drawn under the debacle – but Beingmate was now septic.

2018: losses signal the end

Months of sustained pressure culminated with Fonterra’s half-yearly loss announced this week. Spierings would go (although chairman John Wilson denied it had anything to do with the result), and its Beingmate investment was written down by $405m.

Jilnaught Wong, professor of accounting at the University of Auckland Business School, said the $405m write-down could look like this: Fonterra’s share of Beingmate’s 2017 full year loss was $41m. If this kind of loss continued, at a 10% yield, this equates to a $410m destruction in the value of Fonterra’s investment in Beingmate.

So what has been the damage to shareholders? A simplistic way of looking at the cost of this disastrous investment would be that Fonterra spent $756m on the investment and it is now worth $244m, so it lost $512m. But it’s worse than that, because all investors expect a return on their money.

If their expectation was, say, a 10% return per year, the carrying amount of the investment, (assuming no dividends have been received), at 31 January 2018 should be $993m, not the $244m fair value. “Looked at it this way, the loss to shareholders is $749m – not half a billion dollars, but three-quarters of a billion dollars.”

He said the board, CEO and management team have effectively destroyed about 10% of shareholder funds (available before the Beingmate write down and the Danone arbitration), and the investment leaves more questions than answers. Why did Fonterra buy a minority stake in a Chinese company, knowing the drawbacks of being a minority shareholding? Who was keeping an eye on its investment?

“Hopefully, the Fonterra board and executives will be pondering these questions. Lessons, if any, have been very expensive,” the professor said. Indeed.

The Spinoff’s business content is brought to you by our friends at Kiwibank. Kiwibank backs small to medium businesses, social enterprises and Kiwis who innovate to make good things happen.

Check out how Kiwibank can help your business take the next step.