In our Q&A series, The Lightbulb, we ask innovators and entrepreneurs to tell us about how they turned their ideas into reality. This week we talk to Fraser McConnell, co-founder of alternative payments app Choice which is currently running a two-week pilot phase with Wellington bars, restaurants and cafes.

First of all, give us your elevator pitch for Choice.

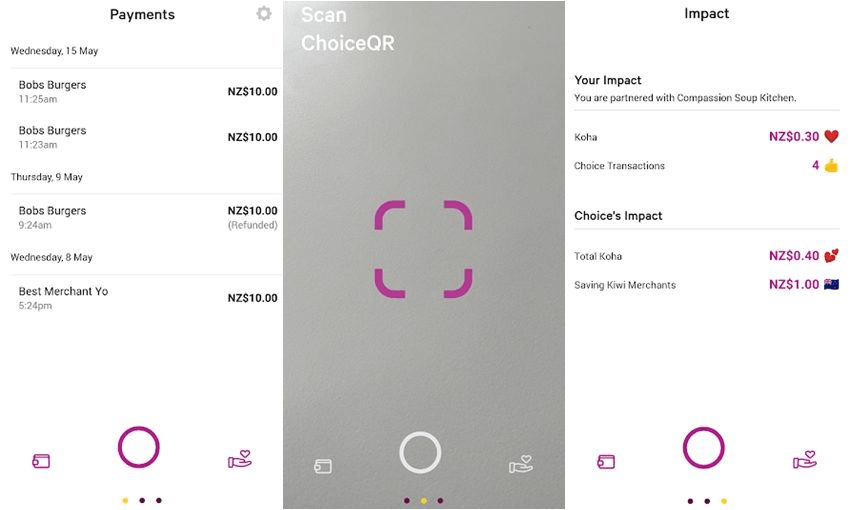

Choice is a payments system that allows anybody to pay with their phone rather than a bank card. They scan a QR code on the terminal of the counter of the store, reducing the merchant’s transaction fee from what can be a 3% fee all the way down to a 10 cent flat rate fee.

[By using Choice] we then give half of that transaction fee (5 cents) to charity. So every time you pay you can pay with purpose. We’re bringing the barrier to entry for making a positive difference down to zero. Anybody can make a difference with Choice. It doesn’t cost you anything as a consumer.

What were you doing prior to Choice? How did you and co-founders Ossie Amir and Alex McCall meet?

Alex and I co-founded Squawk Squad together and we’ve also started a bunch of other startups here and there. We go all the way back to university.

We didn’t meet Ossie (Carbon Valley, Jrny) until we started Choice. He came in very much as a systems thinker [while Alex and I were] more mobilisers of crowds. By combining the two, we found a really sweet spot in the middle.

So how did the idea of Choice come about? What was your lightbulb moment?

We were inspired by the blockchain space in the beginning. All three co-founders had been involved in the blockchain progression from as early as 2014. However, there was a lot of hype and talk about this fantastic technology, but not a lot of follow through. So we asked ourselves: how can we actually create something useful and impactful? Something that could help society?

We then looked at where waste was happening and that was when we stumbled upon the payments space. [This waste] happens due to what’s essentially a duopoly of payments giants running 82% of the cards market. We then asked ourselves: ‘If there wasn’t such a barrier to innovation in this space, how might we open it up?’ That’s the angle we came in on, and when we realised we could do that as well as impact local communities in the form of charity, that’s when we really hit our stride.

We were seeing two extremes. One extreme was over half a million dollars leaving New Zealand merchant pockets every single year [and the other were these] global societal issues. For example, we see in our backyard that 80% of our bird species are threatened with extinction. We’ve also got the highest youth suicide rate in the developed world, and on top of that, one in three children are below the poverty line.

We wanted to [find a way of] redirecting one extremity of wealth back to the local communities in need in a Robin Hood type fashion. But we also wanted to create a new, more efficient system that kept more money within our economy.

Can you expand on what you mean by transaction fees?

To understand the current fee structure for cards, it’s difficult because when you ask a bank for what it is, they’ll give you this big matrix, this big ugly thing that even merchants don’t entirely understand. They often don’t know what’s going to get pulled out of their accounts at the end of the month because it’s completely convoluted. So merchants might be paying as much as their electricity bill [in transaction fees] but with even less predictability.

Typically, a higher end fee is 3%. This is a compounded fee from what might be debit or credit fees, and then as soon as you add Tap & Go/Paywave, it increases that fee as well. That’s why you see all those ‘No Paywave’ stickers over New Zealand terminals because stores aren’t willing to add extra money or direct those fees to their consumers.

Basically, contactless payments are holding merchants at ransom. They don’t have a better option and Choice is coming in and saying there’s a better way to pay, we’re going to charge you a flat fee, and it’s going to be reduced significantly. So instead of paying maybe $3, it’s going to be 10 cents.

Where do these fees go?

Electronic card transaction fees go to your card payments companies (i.e. Visa and Mastercard) or they go to banks as interchange fees. So in New Zealand, they’re essentially going offshore.

So other than the fact that half of the transaction fee goes to charity, what’s the incentive for consumers to use Choice?

Firstly, we’re keeping money in New Zealand by charging merchants a lot less. We’re making it more efficient, we’re saying we can do this at a much more reduced cost, and at the same time, we’re giving half of that fee away to charities.

We’re able to undercut costs [because] the real innovation of Choice is that it’s not a payments app. A payments app is just the form its taking at the moment. But the real innovation is we’re creating a completely new realm separate from the likes of Visa and Mastercard. So if you think Google Pay and Apple Pay are innovative, they’re just charging a licensing fee on top of the fee that already exists. They work with the card schemes and just add more cost to the merchants. This isn’t helping the payments ecosystem and this isn’t helping small and medium sized businesses, especially not in New Zealand.

Instead, [we’re looking to] create a direct connection between the merchant’s bank account and the consumer’s bank account, rather than having to go through a cards system which is basically just a middleman anyway.

[For our pilot phase], we’re connecting with customer cards. However, everything is still operating at our $0.10 merchant transaction fee due to a technical connection that we’ve made. This allows us the short-term pilot trial and our next releases will be with bank APIs.

With Choice, consumers can choose which charities half their transactions fees go to. What charities do you currently work with?

For our pilot launch, we’ve had just one charity partner (Wellington’s Compassion Soup Kitchen) just to make it simple. However, we have some partner charities for further launches which include the likes of Starship Foundation and Kiwis for Kiwi.

What incentive do merchants have to use Choice? Are there any other costs for them other than the 10 cent flat rate fee?

Nope, so it’s really simple. You don’t have to pay subscription fees or anything like that. [And because we use QR codes], merchants don’t need to have another terminal on their counters.

The incentive for merchants is twofold. One is to save money from their bottom line. Like I said, we have a dozen merchants across Wellington currently transacting with Choice who are thrilled to finally have something like a ‘retaliation’ against Paywave and Tap & Go because they’ve never had an alternative option. We’re providing them with a means of saving money from their bottom line instead of being charged unjust fees. Choice is also a contactless system. It’s just as fast as Paywave.

Second, they get to champion these charities as well and get to see money going to charities from these payments rather than going to the back pockets of international card companies.

How much have you redirected to charities so far in your pilot phase?

After a week (May 24 – June 5), we’ve had more than 500 user signups, 400 transactions, and $22 go to Wellington’s Compassion Soup Kitchen. Although that might seem humble, that’s over a short period of time with just 12 merchants. Looking at the bigger picture, if we enabled this across New Zealand, [we can estimate that] $90 million could be redirected to charity, and that’s just in New Zealand alone.

The metric we’re really excited about though is the number of people changing their payment behaviour. The big goal is to have 50% of active users use Choice twice or more, and after a week, we’ve had 47% of users using Choice again.

What’s been your biggest challenge so far?

The real challenge so far has been working with banks, which isn’t so surprising.

Basically, to enable [the next phase of] Choice, we’re [dealing with] open banking which is a global movement. Yet banks [have been far too slow to] provide access to their APIs. Banks like to think they’re moving quickly and we have some incredible relationships with them, but they’re stifling innovation in New Zealand, to put it simply. They think they’re opening up their doors and they like to say they’re working really close with regulators so they look good. But the fact of the matter is they’re stifling innovation for small Kiwi fintechs, which are minuscule compared to their enormous size.

So the plan is to eventually connect bank accounts directly. Are you able to say what banks you’re looking to partner with?

At the moment we’ve got other ways of doing it, but in the long run, we want to be able to connect all bank accounts. It’s stalling from the banking industry that’s slowing us down.

I can’t say which banks we’ve partnered up with yet, but we’ll reveal that in our following launches.

Finally, what can we expect for the rest of 2019?

In a year’s time, we’ll have a beta launch release. There’ll also be some deployments with large retailers and it’ll all be heading towards a national rollout. That’ll all be in late 2019-early 2020.