Alcohol is the latest item consumers are using buy-now, pay-later schemes to purchase. But a bigger problem lies underneath.

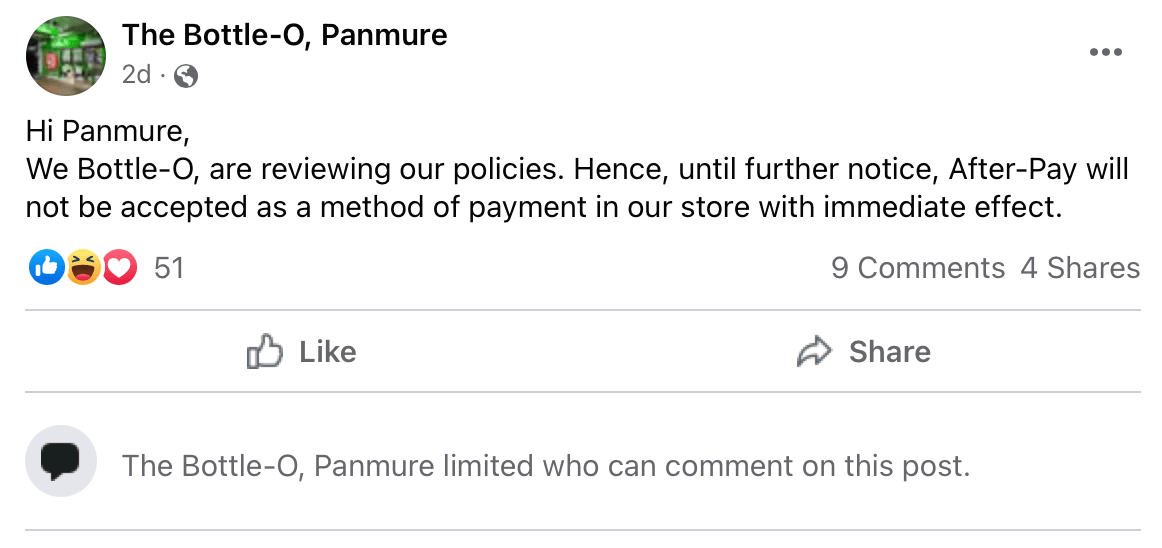

Last Friday, after receiving a torrent of complaints, a Bottle-O liquor store in Auckland’s Panmure announced that “until further notice”, buy-now, pay-later provider Afterpay was no longer available as a payment option “with immediate effect”. In a win for advocates concerned by the combination of alcohol and short-term credit, the u-turn comes nearly a month after the store declared the “wait is over” by proudly announcing its acceptance of Afterpay.

But the fact that bottle stores are even allowed to accept the latest unregulated form of credit has Ngā Tāngata Microfinance Trust chief executive Natalie Vincent worried more harm could befall debt-ridden consumers if action isn’t taken quickly.

Buy-n0w, pay-later, or BNPL, is a fast-growing form of credit allowing people, either in-store or online, to purchase goods or use services immediately and stagger payments in equal instalments across one to three months. Late fees of typically $10 are charged for every missed repayment. Providers like Afterpay, Laybuy and Humm usually make money by charging participating retailers a fixed fee or a percentage of the price of the good or service.

The Bottle-O in Panmure backtracked on accepting Afterpay after store owner Ketankumar Satpute was subjected to online vitriol in response to updating customers on the store’s Facebook page. A screenshot of the post circulated on Twitter, with users expressing concern. One wrote, “unless there are booze trucks trawling our streets[,] this is as bad as booze business gets”. In a follow-up Facebook post, the store said it was reviewing its policies.

Ngā Tāngata’s Vincent leads an organisation providing low-income whānau with small interest and fee-free loans, along with access to a support network of independent financial mentors. She knows too well the pitfalls of BNPL, including that New Zealand’s laws don’t recognise it as a form of credit – the rules requiring credit card and loan providers to look into an applicant’s creditworthiness to ensure they can meet their financial obligations don’t apply to this new, innovative credit alternative.

Another risk of BNPL is how quickly users can get into unmanageable debt. Vincent says three Ngā Tāngata clients collectively owed $2,000 to BNPL providers, two of which had passed the debts onto debt collectors whom Ngā Tāngata repaid. Another applicant had accounts with four providers and was required to make 16 repayments a month. In 2021, the trust started asking applicants to disclose the extent of their BNPL indebtedness.

The credit schemes are already offered for craft beer and natural wine, and listed on Afterpay’s website are Thirsty Liquor Tauranga, Premium Liquor, Merchants Liquor Queenstown and Containerdoor. Vincent says it’s novel in Aotearoa that BNPL is entering the everyday liquor retail market of beers, wines, premixes and spirits to which those stores cater. She found out about Bottle-O on Thursday night, when a friend sent her a screenshot of the Facebook post, and was horrified. Society can’t go any lower than encouraging BNPL debt – a “social scourge” – on alcohol purchases, she says. “Alcohol… is not a necessity of life. We should be ashamed this is allowed to go on.”

But it’s not the store owner’s fault, Vincent says. The fact liquor stores are allowed to accept it is a bigger issue. While BNPL providers have dedicated teams to help users get back on track with their repayments, addressing the risk of financial hardship caused by BNPL is something the Ministry of Business, Innovation and Employment (MBIE) is still deliberating on. Submissions on the discussion document closed in December 2021, and the ministry is considering the feedback. On Friday, a spokesman for commerce minister David Clark told One News he would take recommendations to cabinet “soon”.

The ministry’s accompanying survey shows:

- 44% of nearly 1,800 respondents use BNPL at least every fortnight and three-quarters have more than one provider;

- about 90% have other debts in addition to BNPL;

- nearly 80% use BNPL when they can’t afford a product’s full price;

- almost 90% use BNPL to purchase clothes and shoes while nearly half use it for everyday items; and

- one in five people has missed at least one instalment.

In a survey by the trust, nearly a quarter of Ngā Tāngata clients reported using BNPL to buy groceries, with some commenting that rising food prices have increased their supermarket bill. “To allow this to happen for any consumable purchases, with no regulation…it’s unacceptable,” Vincent says. “But to allow them to purchase alcohol with it is a disgrace.”

In Australia, the connection between BNPL and alcohol is striking. Researchers at Victoria’s Deakin University are investigating the different methods people use to buy alcohol, and experts are already concerned the shift toward BNPL could lead to “financial hangovers”. In late 2021, hospitality operator Australian Venue Co partnered with Afterpay to roll out the scheme across its more than 180 pubs, restaurants and bars, sparking fears debts could balloon out for Australians already under financial strain. The same fears exist in the US, where cash-strapped consumers facing rising living costs are turning to BNPL to purchase fuel, groceries and their daily coffee. In the UK, over a third of consumers believe BNPL has become more appealing since living costs started to climb.

New Zealand’s alcohol industry is back in parliament’s sights after Auckland Central MP Chlöe Swarbrick’s members’ bill to amend the Sale and Supply of Alcohol Act 2012 was drawn last week. The law change proposes abolishing appeals processes on local alcohol policies, prohibiting sponsorship and advertising in an effort to remove the link between sport and alcohol, and reducing young people’s exposure to such messaging.

While Ngā Tāngata’s CEO isn’t across all the details of Swarbrick’s bill, Vincent supported the proposal. “Banning alcohol sponsorship for sports and things, it’s a no-brainer,” she says. “With buy-now, pay-later, [you] don’t even need to have the cash so we’re making it even more accessible.” Urgent action is needed, with the latest example “shining a light on the potential harm”, Vincent says. “Buy-now, pay-later debt is a social scourge. It’s burdening more and more people with problem debt. We see it every day.

“It’ll only be five minutes before more and more liquor stores around the city and around the country are doing the same thing. Every day, there’s more and more potential for harm if we don’t actually act quickly and do something about this.”