Priced out of the housing market? Don’t lose heart. In the second part of a series on alternatives to property investment for ‘Generation Rent’, Jenée Tibshraeny explains the benefits of passive investment and offers a comprehensive guide to the available options.

This story has been updated since it was first published on interest.co.nz in June. Read part one of the series, on property investment with friends, here.

Can you relate to this?

You have $5,000, $30,000 or $150,000 sitting in a savings account.

You’re keen to invest it, but don’t have the knowledge or inclination to trade shares in individual companies yourself. Plus, you’re all about diversification, so don’t want to put all your eggs in a few baskets.

You could hire someone to buy and sell shares for you, but you realise this is too expensive unless you have hundreds of thousands of dollars to invest.

You could invest in a managed fund, much like many KiwiSaver funds. However you need to be willing to pay more in fees to have a fund manager constantly move your money around in an attempt to maximise your returns. If you go down this route, you need to believe your fund manager can outsmart the market.

If you’re of the mind this isn’t possible, or the fees you pay to use a fund manager outweigh the higher returns you’re expected to receive, investing in funds that simply track the market could be the way to go.

Big picture stuff

There is a raft of material out there that debates managed versus passive investing. I won’t wade into this argument now.

But when you do your own research, you should remember New Zealand has a very different market to the US, where a lot of financial literature comes from. Investing in index-tracking funds is much cheaper in the US due to there being more competition, economies of scale and investors having greater access to markets. You may consequently not save as much in fees going down this route as people like passive investing evangelist/life coach Tony Robbins may have you believe.

Another thing to be mindful of when considering investing in index-tracking funds is that the market has been performing well since the 2008 Global Financial Crisis. So people you talk to who have gone down this path in the last 10 years are likely to be boasting about their returns.

The question is whether they can sit tight and ride out the wave when the market turns and the values of their investments fall, while their mates with managed funds possibly suffer softer blows.

Some of the newer index-tracking products available in New Zealand haven’t yet seen a major downturn, so are essentially yet to be tested.

Getting into the detail

With this in mind, if you see merit in passive investing, this second instalment of my Generation Rent Investment Guide is for you.

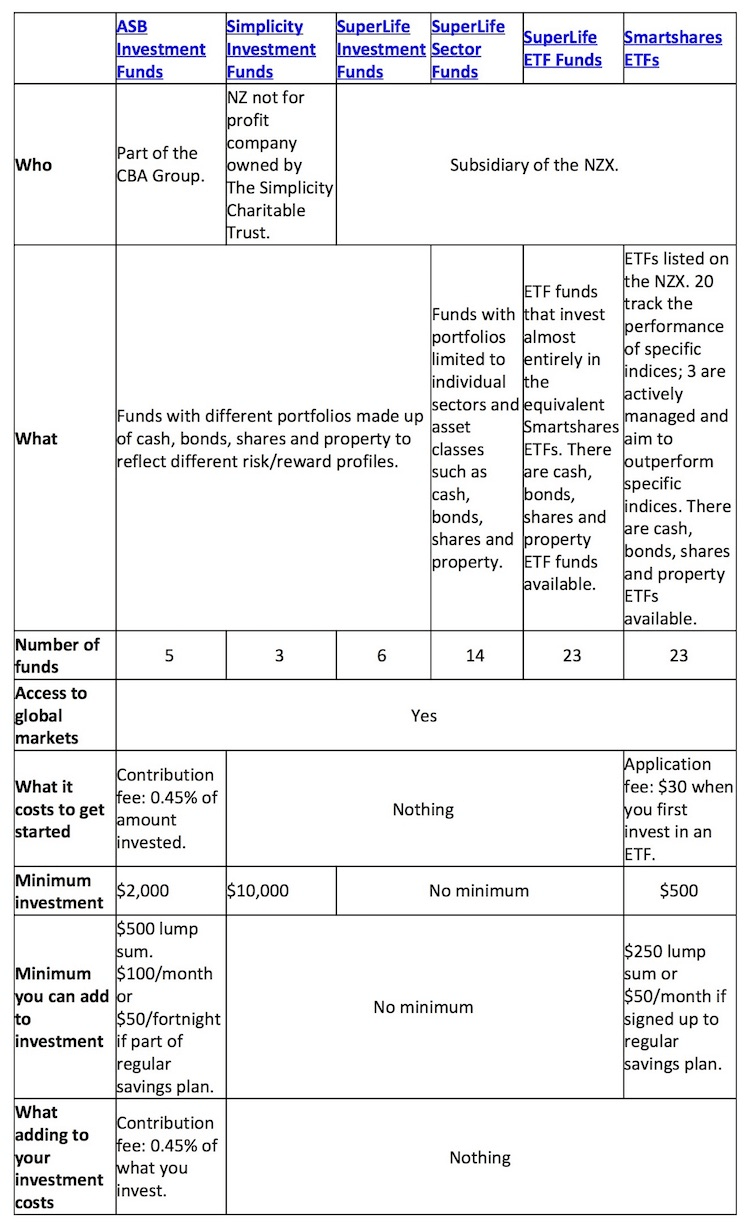

I have put together a table comparing the nuts and bolts of a few products that enable you to do so.

Product disclosure statements: ASB; Simplicity; SuperLife; Smartshares.

Here is my take on the various options:

Investing in a fund with a set portfolio vs going down the Exchange Traded Fund (ETF) route

Putting your money in an investment fund through the likes of ASB, Simplicity or SuperLife enables you to let the experts do the work to put together a portfolio with an asset mix that matches your risk/reward profile – much like when you invest in a KiwiSaver fund.

If you think you’re capable of putting together a portfolio that gives you the right level of diversification and exposure to risk, ETFs or SuperLife’s sector funds may be appropriate. These options give you flexibility and agility, which could be useful if you understand the market and have a clear strategy.

All of the options can be used as longer-term savings vehicles, in that you can make regular contributions to your investments. ASB will however charge you a 0.45% contribution fee.

The other general difference is accessibility. None of SuperLife’s products require you to have a certain amount to invest. You only need $500 to invest in Smartshares ETFs, $10,000 to invest in Simplicity’s investment funds and $2000 to invest in ASB’s funds.

Show me the money

This is where things get really difficult.

Ideally when comparing returns across products designed for longer term investors, you should look at what their annual rates have been over a number of years. The problem is many Smartshares ETFs, as well as Simplicity’s funds, haven’t been around for that long, so don’t have a track record.

You can therefore only make a fair comparison using returns over the past year, as I have done below. Remember returns can vary a lot over a six-month period, let alone a 10-year period.

It is also difficult to compare returns, as different products have different compositions, so you’re never quite comparing apples with apples.

Nonetheless, I believe there’s some value in looking at the extent to which returns may differ and how various fee structures affect your return.

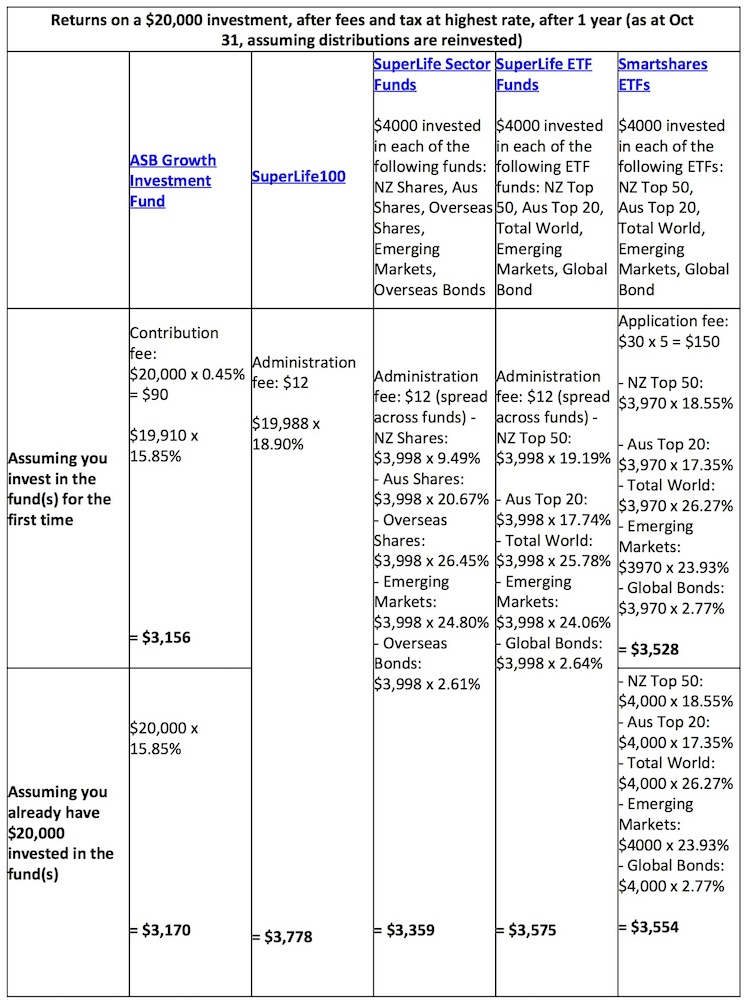

So I have done what I have been advised not to do, and created ETF, ETF fund and sector fund portfolios that somewhat reflect the composition of SuperLife and ASB growth funds, to do a comparison. I haven’t included Simplicity as its investment funds have only been available to the public since April.

Smartshares ETFs vs SuperLife ETF funds

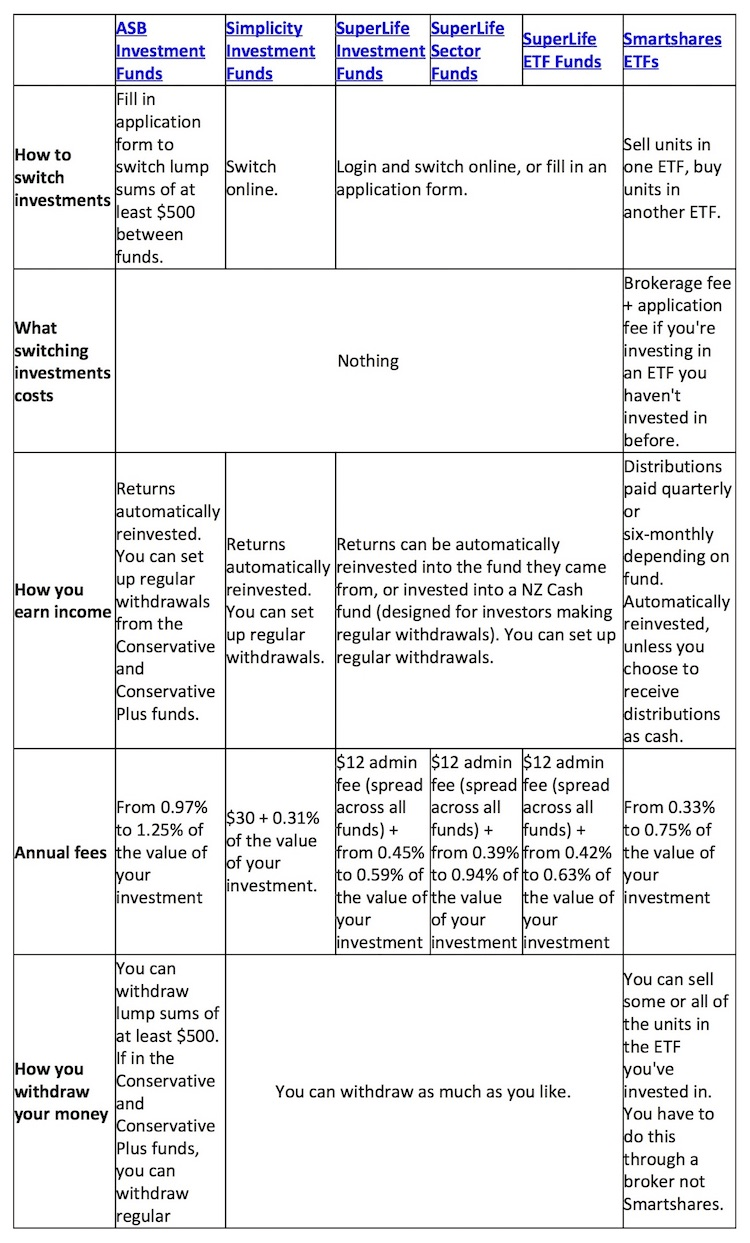

As you will see, there is around a $30 difference between the returns you would have received over the past year if you bought units in Smartshares ETFs yourself, compared to if you did so through investing in corresponding SuperLife funds.

NZX Head of Funds Management Aaron Jenkins says there will always been a minute difference because SuperLife’s ETF funds include a bit of cash, as there is a delay between people investing in the funds, and SuperLife buying the ETFs.

Furthermore, the fees differ a little due to the buying power SuperLife has as it buys ETF units on behalf of a number of investors.

The other difference between investing in Smartshares ETFs directly or through SuperLife is that you have to pay brokerage fees if you’re trading ETF units on the stock exchange yourself. ANZ and ASB Securities provide online brokerage services, with the latter being cheaper.

Therefore, investing in ETFs through SuperLife may be better for a more active investor. However Jenkins says people investing in ETFs are generally playing a long game, so aren’t too fixated on doing a lot of trading.

Throwing SuperLife’s sector funds into the mix, Jenkins says the appeal with these is that they’re a simplified version of ETFs. So this might be the way to go for someone who wants to invest in a range of New Zealand shares, but doesn’t know whether it’s best to invest in a NZ Top 10 or Top 50 ETF, for example.

The fees across Smartshares ETFs, SuperLife ETF funds and SuperLife sector funds are fairly similar.

ASB vs Simplicity vs SuperLife investment funds

As with the three investment options discussed above, the returns you can expect to receive from investment funds that largely track the market, should theoretically be quite similar.

The make-up of their portfolios are fairly standardised across different risk profiles and therefore one is broadly expected to be as affected as another when the market shifts.

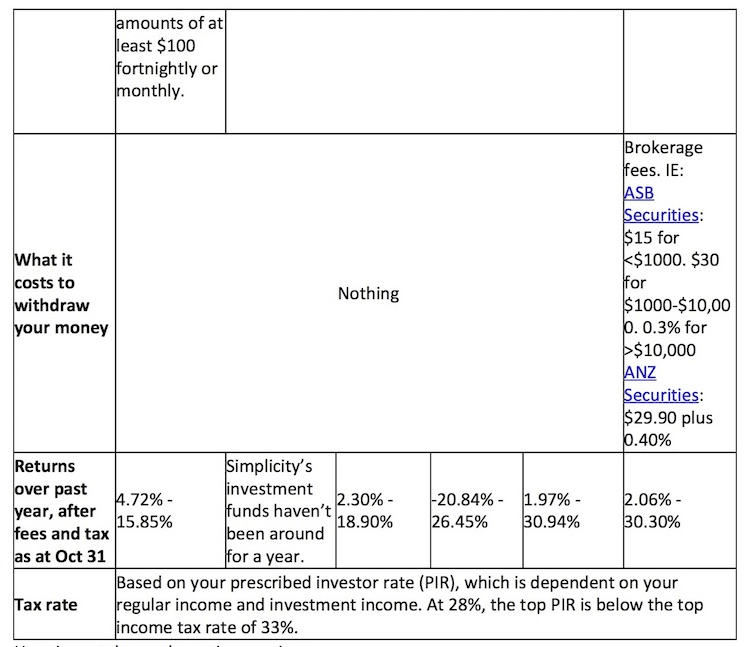

While the annual returns (after fees and tax) of ASB’s investment funds have ranged from 4.72% to 15.85%, over the last year, SuperLife’s have ranged from 2.30% to 18.90%.

Differences are partially derived from fees. ASB’s range from 0.97% to 1.25% p.a of the value of your investment, while those for SuperLife’s investment funds range from $12 + 0.45% to 0.59%.

Simplicity has marketed itself as having the lowest fees in the market, setting a standard annual fee across all its funds of $30 + 0.31% of the value of your investment.

Furthermore, being a not for profit, Simplicity has vowed to pass on the gains it gets through economies of scale to its investors, by dropping fees when it can.

Its managing director Sam Stubbs says since launching in September last year, $286 million has been invested in Simplicity’s KiwiSaver and investment funds. The organisation will break even once funds under management hit $400 million.

While this innovative business model is appealing, I would be interested to see what Simplicity’s returns look like in a few years’ time.

Finally, there is an argument that you’re better off investing in an established institution with backing from a larger parent company like the NZX or CBA. However Stubbs says all the money you invest through Simplicity is held by the Public Trust, so will be protected if Simplicity goes belly up.

Final two cents

I have only scratched the surface of this topic, but trust this article has given you an idea around what’s out there and how various products differ.

While I have drawn my conclusions having studied product disclosure statements and talked to the NZX’s Head of Funds Management Aaron Jenkins, Smartshares Product Manager Dean Anderson, Simplicity Managing Director Sam Stubbs, Simplicity Head of Operations and Compliance Craig Simpson, ASB spokespeople, and financial columnist Mary Holm, among a few other experts, please remember I am a financial journalist, not a financial adviser.