The pension probably will still be around when today’s youth retire, but refusing to change the system at all will mean a tougher working life, writes Jenesa Jeram.

It’s hard to make young people care about New Zealand Superannuation.

I should know. Even when confronted with David Seymour’s warning that “NZ baby boomers are building a banana republic, and no one gives a shit,” I admit, dear reader, that I was one of those people who did not give a shit.

Young people have been told NZ Super is unaffordable, and many are preparing for a future without it.

Yet we are simultaneously told NZ Super is a political hot potato, and that the major political parties are reluctant to touch it. National did bite the bullet before the last election and proposed to raise the pension age incrementally, but even that policy has been reversed by Labour.

The New Zealand Initiative set out to reconcile these two seemingly conflicting observations in our recently released report, Embracing a Super model: The superannuation sky is not falling. If we are truly hurtling towards disaster, why is it so difficult to convince our elected government to act?

The sky is not falling

As the title suggests, the Initiative’s take on NZ Super is not all pessimistic. We don’t need to infiltrate a Grey Power meeting to find out why the public, and our politicians, hold NZ Super in such high regard.

There are a lot of things to celebrate about the model.

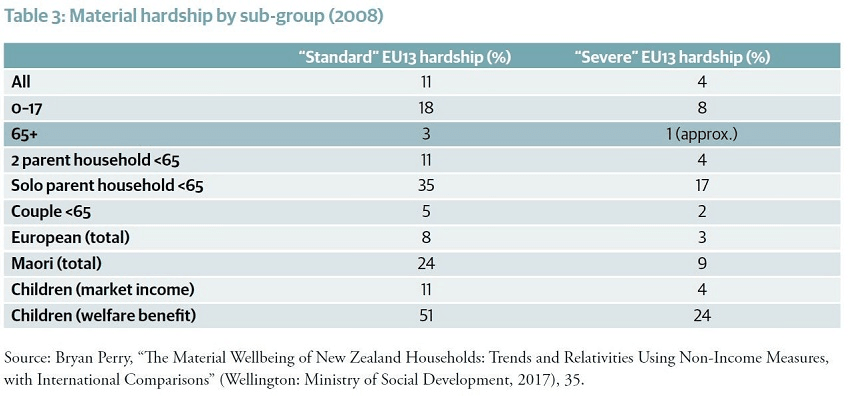

In 2015, NZ Super provided nearly all the income for the poorest 40% of the elderly population. Despite many people being wholly reliant on this one source of income, the material hardship rates for the elderly are low.

We have very low hardship rates for the elderly compared with other groups in New Zealand, and one of the lowest compared with European countries.

New Zealand is one of a handful of countries in the world to provide a universal non-means-tested pension, payable from the age of 65 until death. Some people believe such universalism is unsustainable. But it may actually save us money. NZ Super does not distort incentives for employment and savings as much as means-tested systems, and it has lower administrative costs.

Despite claims to the contrary, NZ Super is also relatively cheap.

The cost of our pension system as a percentage of GDP is lower than most OECD countries (but note that these countries are ageing at different rates and have different demographics). Though people worry about the projected costs of NZ Super in, say 2050, it should be appreciated that many countries are paying that amount or more today. Some countries are struggling under the fiscal strain, but other countries like Denmark, Finland, Norway and Sweden often attract acclaim for their pensions.

NZ Super is successful in keeping the elderly out of poverty, it is simple and efficient, and it is relatively cheap. So why are people panicking?

Treasury tells us what might happen if everything stays the same

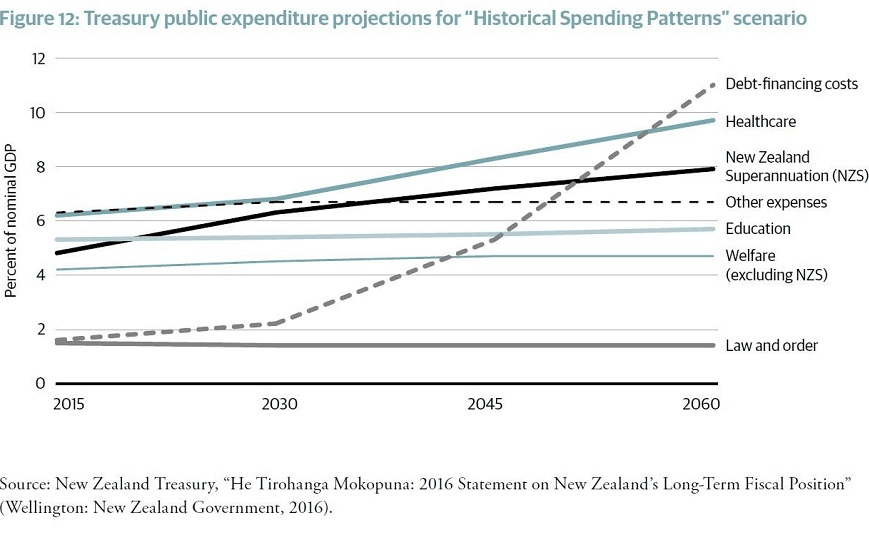

When experts and commentators talk about NZ Super being unaffordable or unsustainable, they likely have Treasury’s fiscal projections in mind. A simple eye-balling of the projected fiscal costs does reveal a distressing future.

As the populations ages, gross healthcare and NZ Super costs will rise from a combined 11% of nominal GDP today to nearly 18% of GDP by 2060. Debt financing costs alone could rise from 1.6% of nominal GDP today to 11% by 2060. Debt of that magnitude would surely plunge New Zealand into a fiscal crisis.

Considering these numbers, it is hard not to think of economies like Greece, Italy and Portugal, which are now struggling to meet the fiscal demands of an ageing population.

Keep in mind, though, that these projections are a ‘historical spending’ scenario, based on a set of assumptions that will not eventuate. The scenario assumes public spending and tax revenue trends will continue, and that the government will not respond to deficits and debt.

But there is one thing working in New Zealand’s favour that could mean we do not suffer the same dismal fate as many other ageing economies. The Public Finance Act sets expectations for prudent debt management, and is therefore a safeguard against vicious debt spirals that would see debt-financing costs balloon.

Assumptions about tax revenue and economic growth matter too. For example, though the gross projected cost of NZ Super is around 8% of GDP in 2060, the cost once taxes are paid on NZ Super (net cost) reduces to 6.7% of GDP.

This is also where productivity growth becomes vital. The rising costs of NZ Super and healthcare are represented as a proportion of GDP. Faster rates of productivity growth relative to increases in the real interest cost of government borrowing can allow increased government spending without falling into ballooning debt.

We know that the costs of NZ Super and healthcare will rise, but we don’t yet know future economic growth rates, tax revenue, or labour market conditions.

The sky is not falling, but it is not clear skies ahead either

At this stage, it is unrealistic to conclude that there will be no NZ Super available for today’s young people by the time they retire. As with the old saying about babies and bathwater, it would be a shame to completely do away with a model that works reasonably well.

But equally, young people need to be aware of the real future costs of keeping NZ Super as is.

Though New Zealand has safeguards against toxic debt spirals, managing fiscal prudence means decisions must be made around spending and taxes.

Productivity growth will be an important means of reducing the future costs of public services relative to incomes, but it is unlikely that productivity alone will be enough. Tax revenue will need to rise, and/or spending on other public services will need to reduce to meet the shortfall between spending and revenue.

A refusal to touch NZ Super could mean a tougher working life because of higher taxes paid. Is NZ Super worth paying for if it means less food on the table today? Keep in mind that nothing – not even the NZ Super Fund – secures the future of the model. Governments can change the model at will.

Other aspects of the welfare system also need to be considered. After all, $1 spent on NZ Super is $1 that cannot be spent elsewhere. As the population ages, there will be less money to support those most in need. Supporting the elderly is important, but so is alleviating child poverty and raising the living standards of the working poor.

And what about other public services? At about 8% of GDP by 2060, is the proportion of taxpayers’ money going towards NZ Super desirable, given spending on welfare (4.7% of GDP) and education (5.7% of GDP) is much lower?

Even if the public were to conclude that the current and future spending on NZ Super are about right, could they say the same about current spending on other public services like education and health? The Treasury’s fiscal projections might get a lot more scary if spending on other public services rise too.

Why young people should give a shit

One of the problems with talking about the ‘affordability’ of the model is that it does not give young voters a call to action. If the NZ Super model is affordable, then there is nothing to worry about. If it is unaffordable, then all we can do is throw our hands up in despair and wait for the sky to fall.

But if the problem is instead how to spend scarce public resources, then young voters have decisions to make. This is not just about NZ Super, but also about the quality of our working lives and ensuring that those who are struggling can get the support they need.

There are small changes that can be made to the NZ Super model to preserve its best bits while addressing some of the concerns raised above. Crucially, The New Zealand Initiative recommends raising the pension age and linking it to health expectancy; and re-indexing NZ Super to inflation rather than wages and inflation.

We recommend signalling any changes well in advance to give people time to financially prepare, and to ensure people close to retirement are not disadvantaged by any announced changes.

The problem is that even small changes are resisted by some voters, and such resistance might only get stronger as the voting population ages. And let’s be frank, some of the voters most resistant to change are current superannuitants or those nearing retirement who worry that someone may take away their “hard-earned” pension. No one is suggesting that.

Others are resistant to change because they believe they paid taxes all their working life with the expectation of securing their pension in the future. But as I explained above, there is nothing written in stone to guarantee NZ Super will always remain in its current form.

Fixing the roof while the sun still shines will give governments and the public more choices in the future. Young voices should not be drowned out by those who already have their shelter sorted by the time the grey clouds set in.

Jenesa Jeram is a research fellow at The New Zealand Initiative and the author of Embracing a Super model: The superannuation sky is not falling, which you can download from the Initiative’s website.