As Australian banks make more and more money in New Zealand, they contribute less and less to the economy, says Sam Stubbs. Here’s what we can do about it.

The Australian banking inquiry has been the greatest scandal in Australian corporate history. Heads are rolling, fines being handed out and criminal charges laid. And it’s far from over yet.

At the core of the problem has been the huge profitability of the Australian banks. It has encouraged behaviours which have been horrible for consumers.

Economists call this behaviour ‘rent seeking’ – extracting ever more from the economy without adding to its well being. Anyone doubting this should spend a day listening to the Australian inquiry.

Is the same thing happening in New Zealand? The numbers would suggest yes, because:

- Banks make more money relative to GDP in New Zealand than in Australia

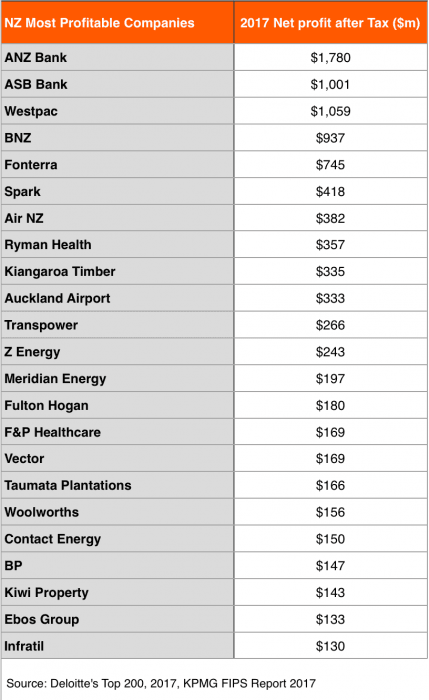

- Ranking New Zealand company profitability, the Australian banks sit at 1, 2, 3 and 4, all well ahead of Fonterra, Spark and Air New Zealand

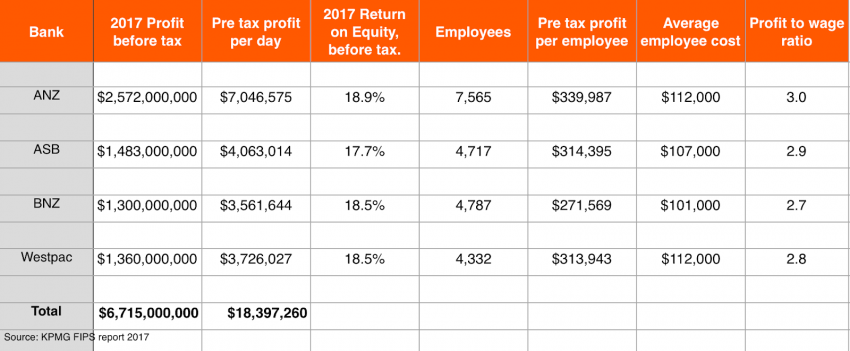

- While employing lots of New Zealanders and paying significant taxes here, they still earn 2.8x more in profits than they pay their employees

Bank profit is essential to the health and running of our economy, but how much and at what cost? The numbers are very revealing.

In 2017, Australian bank profits in New Zealand were 2.8% of GDP vs 2.2% in Australia so they are extracting 25% more in profits from our economy than they are at home. These numbers look shocking next to the 1.4% of GDP banks made in Japan, 1.2% in the US and 0.9% in the UK in 2016.

And while global rankings do not typically include New Zealand, these numbers indicate that our banking system is amongst the most profitable in the developed world. This is not a number to be proud of!

Within New Zealand banks really stand out as profit machines. They rank 1, 2, 3 and 4 in after-tax corporate profitability. No other developed market I’m aware of has banks as the four most profitable companies. Even the runt of the big banking litter, BNZ, made 25% more than Fonterra last year. ANZ made 2.4x as much.

The banks are used to defending their enormous profitability and can quote some impressive statistics for the contribution they make to the economy. The bankers association website talks about them employing over 25,000 New Zealanders, and paying over $2b in taxes.

So let’s look at their profitability last year on a pre-tax basis (which is how profits and investments should be compared) relative to the number of employees.

These numbers are embarrassing for the Australian banks operating in New Zealand. Return on equity for their shareholders averaged over 18% pre-tax last year. This is a high number given how big the businesses are. And their profits were over $18m per day before tax. That’s $750,000 per hour and $1,400 a year for every New Zealander.

And is the average bank employee aware that profits the banks make average 2.8x what they get paid?

It’s clear that a profitable banking system is desirable because a bank losing money is one that is less likely to be lending money. But there such a thing as too much profit, especially when banks are offshore owned.

And this is where New Zealand badly stands out. We’re the only country in the developed world I know of where the banking system is predominately offshore owned. It’s big problem for four reasons.

The first is that it’s natural to milk your overseas subsidiaries if you can, and that is clearly happening here. Massey University has calculated that the profits of the Australian banks in New Zealand have increased 75% over the last decade, while GDP has increased by only 23%. And we’ve already seen that Australian banks profits in New Zealand are a higher % of GDP than in Australia.

The second issue is one of control and destiny. We’re vulnerable to Australian banks scaling back their activities here when things are tough at home. When they get a sneeze, New Zealand customers are more likely to catch a cold. We shouldn’t allow ourselves to be that exposed to decisions made in Sydney and Melbourne.

The third major issue is our current account deficit. Shipping Australian bank profits overseas make the deficit persistently bigger, and it makes New Zealand look like a riskier economy, leading to higher borrowing costs and mortgage rates. Even if the same profits were made by New Zealand owned banks, we would be in much better shape with them retained here.

The fourth reason is the most significant, the loss of all that money into the hands of Australian owners. At 2.79% of GDP, it’s a big number in itself, and an enormous one when you consider what the compounding benefits of that would be if it stayed in the economy.

So what’s the solution? Proper competition, and the sunlight a banking inquiry would bring.

Competition for the Australian banks in New Zealand is too weak. Kiwibank is a start, but hasn’t hampered Australian profits. Hopefully the NZ Superannuation Fund and ACC, as substantial owners of Kiwibank, will properly fund it to be a serious competitor to the Aussies. It’s a golden opportunity to address what is a serious burden on our economy, and a tax on our future prosperity.

We need competition in KiwiSaver too. This is a product for New Zealanders, but 85% of KiwiSaver market share is held by Australian banks. The high management fees they charge are very profitable and support Australian dividends, not New Zealand savers. It’s this lack of competition that was the rationale for establishing Simplicity KiwiSaver, to give New Zealanders a low cost, locally owned, high-quality choice. It’s tackling the Australian model by giving profits back to members, with no aggressive sales strategies or commissions paid.

And we need a banking inquiry in New Zealand. The problem is too big, with too many similarities to Australia. Informed consumers will make better decisions, so let’s inform them the same way the Aussies are, via a Royal Commission of Inquiry. If the banks have nothing to hide they should welcome it. The regulators should encourage it too, as the end game will likely be more resources for them to police an industry so vital to our well being.

To say bank profitability is a good thing is a truism. But to say current Aussie bank profitability in New Zealand is a good thing is just a big white lie. The Aussie banking inquiry has been an ‘Emperors New Clothes’ moment over there, exposing the brutal realities.

We need a similar inquiry here, so similar behaviours, if they have occurred, will be exposed and rectified. Sunlight is the best disinfectant, and we could all be wiser, and richer, for it.

The Spinoff’s business section is enabled by our friends at Kiwibank. Kiwibank backs small to medium businesses, social enterprises and Kiwis who innovate to make good things happen.

Check out how Kiwibank can help your business take the next step.