As winter sets in, it’s worth facing facts: Our houses are heat-leaking mould machines – and we won’t meet our child poverty and carbon zero targets unless something drastic is done to fix them, writes Bernard Hickey.

Follow When the Facts Change on Apple Podcasts, Spotify or your favourite podcast provider.

Back in 2005 when Auckland’s median house price was under $350,000, our family had the good fortune of being able to afford to buy a house close enough to the CBD to cycle to work. It almost felt too good to be true. We discovered during our first winter in the 1920s wooden bungalow on the shady side of one of Tamaki Makaurau’s many volcanic cones that it was too good to be true.

It was bitterly cold and quickly mouldy. Our clothes sprouted furry layers in our dank wardrobes. The roof leaked into the bathroom and a few other places we could never quite fathom. We got coughs and colds we hadn’t experienced before during five winters in a centrally-heated house north of London, including a couple of years when it snowed. It turned out our house was a pristine Auckland original: beautiful native timbers unsullied by insulation or any form of heating, and a roof that looked more like lacework than a barrier against the heavy showers that swept in from the west. We soon plugged in as many heaters as we could afford from The Warehouse and layered up with jerseys and those purple fluffy blankets that smell like plastics factories. We kept them well away from the bar heater.

After two winters and over a dozen electricity bill shocks, we were desperate. Luckily for us, we were home owners and had received the manna from heaven of unearned and leveraged capital gains that gave us the equity we could withdraw from our home to make it a home. We didn’t have to ask a banker for a loan or beg a government department to take pity on us with a grant. We simply used our floating-rate revolving credit mortgage to pay for a new roof, insulation above and below, a heat pump and a ventilation system that pumped the warm air from the roof cavity down into the house.

It was a revelation. Suddenly, it was a nice place to be in the dark months. The colds dried up and we didn’t have to worry about whether our clothes would smell like an old Kiwi villa when we were at work. It was worth it for the sheer impossible-to-value feeling of being warm and comfortable, but the financial journalist in me did the sums after the fact on whether it actually made financial sense and was “paying for itself”.

Our power bills dropped by around $200 a month for six months of the year and we didn’t have to spend around $100 a month on doctors bills and medicines. There might have been a trip to A&E a year we avoided, but that was a “public cost” we didn’t have to bear financially and therefore we couldn’t include in the calculation. A fuller “society-wide” evaluation would have included that cost, along with the less easily measurable benefits over decades of fewer kids in hospital, fewer sick days at work, and a happier and warmer and smilier family.

Back in 2005, it never occurred to me to work out how much carbon we had saved by having a healthier home. Although even now, there isn’t a clear way to price or capitalise that carbon saved.

When the numbers were crunched, it turned out the financial benefits attributable to us making our home habitable in winter were just, and only just, more than the costs attributable to us, which were also lower than if we’d had to finance the cost independently of our mortgage. That analysis also included some minor increase in the house value, although in retrospect we may well have over-capitalised because the real value was in the land on which the house clung to on the side of the hill. That’s another one of the drawbacks of our houses becoming financial assets for storing wealth, rather than productive assets valued for the service they provide for mere humans in the cold, dead of night.

But if the full costs and benefits of our refit had been totted up and properly “financialised” into a society-wide balance sheet, the investment would have easily made sense, even with the higher interest rates that applied in 2005. Hospital admissions cost tens of thousands of dollars. Dozens of sick days a year cost thousands in lost wages, taxes and output. Warm happy families make everyone smile in a hard-to-value wellbeing way.

Back then when Auckland houses cost just five times income (it’s now eleven times income), this problem of unhealthy homes seemed solvable to me, although I realise now I was being a slightly naive older and privileged New Zealander. I hadn’t thought about the economics and incentives for tenants and landlords in privately owned homes. I just assumed that landlords would do the maths and realise they were more likely to keep a valuable tenant for longer and be able to charge a higher rent for a warm, dry home. The market incentives, I thought then, would ensure private rentals were made warm and dry. Back then there were sometimes surpluses of private rentals and rents were stagnant around $320 a week in Auckland.

We all know differently now. The average rent in Auckland is $550 a week and landlords now know there is such a shortage they don’t have to worry too much about whether it’s warm or dry. The cost of these mouldy, cold homes is borne by the state in the form of hospital admission costs, lower productivity, lower GST and lower PAYE.

This is effectively a market failure that required an intervention by the state to maximise the outcome for society, and ultimately, the state’s balance sheet and “profit and loss” statement of the annual budget. The state chose rightly to try to rectify that failure by regulating landlords to insulate rental properties and put in heaters and heat pumps.

But the unnecessarily large carbon emissions embedded in that market failure were also unpriced and unaccounted for in either the state’s balance sheet or the landlords’ balance sheets. Dyed-in-the-wool proponents of the Emissions Trading Scheme would argue the need to reduce emissions would be reflected in higher energy costs that consumers responded to. Good luck detecting that signal amid all the noise of ever-rising generation, retailing and distribution costs.

It could be argued the recent removal of interest as a tax-deductible expense for landlords is at least partly a way to rectify this market failure and get landlords to pay for the future carbon credits New Zealand will need to buy to meet our emissions obligations because of the failure of our housing stock to be energy efficient.

Market failures and aspirational goals

I replayed this 2005 experience in my head when reading the Climate Commission’s final carbon budgets for the government last week. It airily suggested more energy efficient homes could play a major role in our path to carbon neutrality.

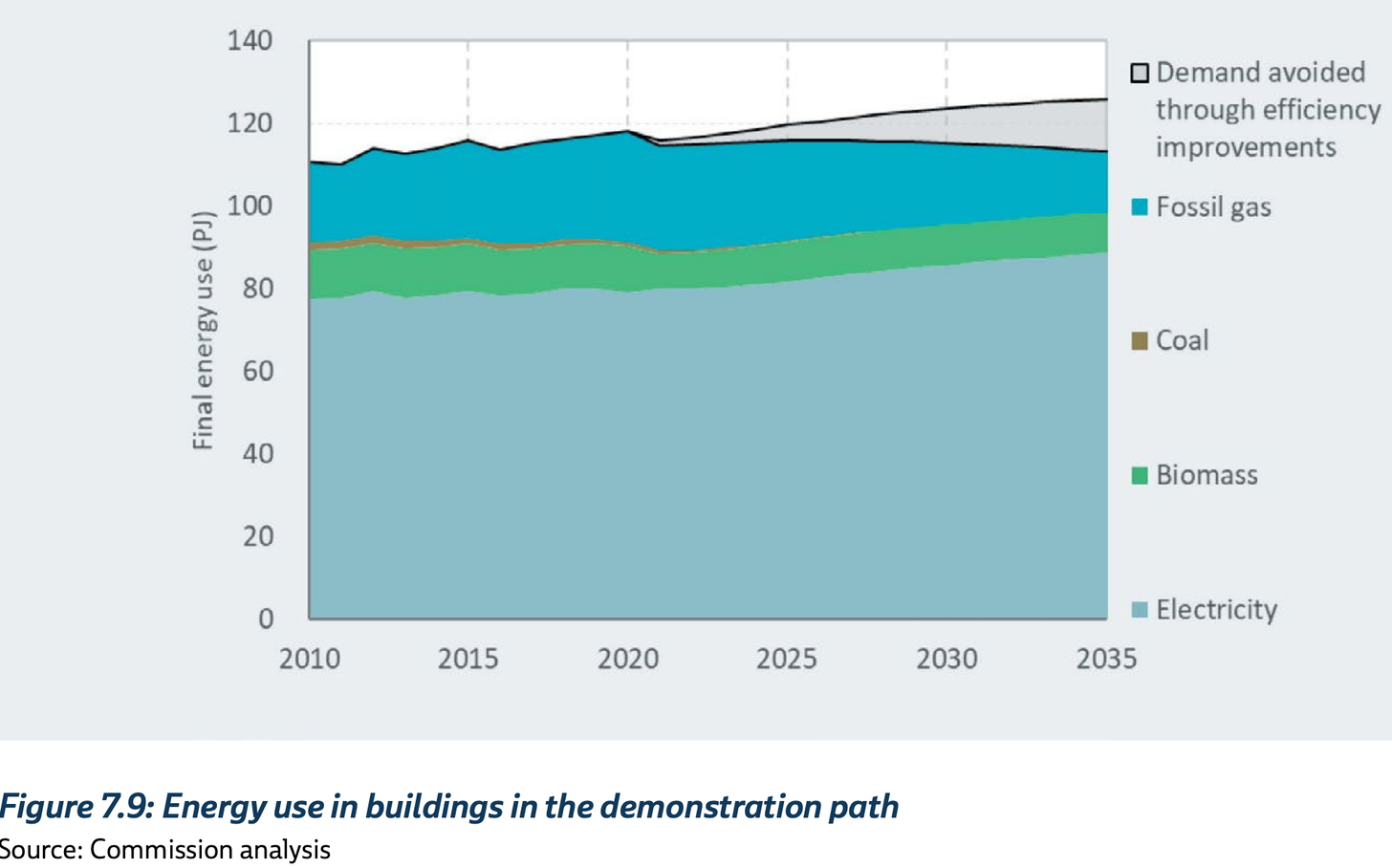

“We assume that the heat demand for existing homes reduces by 6% by 2035. We assume newly built homes require 35% less heating compared to today’s performance,” the Commission said as it published this chart.

In this week’s When the Facts Change podcast I talked to Philippa Howden Chapman, New Zealand’s preeminent researcher into healthy and energy-efficient homes.

She told me the current state of the housing stock – even with the healthy homes regulations – and the way our new homes are built mean New Zealand is currently way behind this prescribed curve.

She is frustrated with the slowness of the rewrite of the building code, which would require builders to always use more energy efficient materials and ensure homes don’t leak warmth, but also are well ventilated to ensure they don’t drown from the inside out.

Market failures abound

The future carbon credits we’ll need to buy to meet our targets are not included in the pricing and choices of building materials and building techniques used by most of our house builders.

Our financing practices and incentives also don’t take into account the embedded carbon deficit, let alone the health, wellbeing and productivity costs of unhealthy homes.

Banks are typically most focused on lending to owners of existing standalone homes in the suburbs. It’s no accident the advertisements for mortgages usually involve some unbelievably young and “average” couple collecting the keys to their new villa in the leafy suburbs and ushering their toddlers into the backyard past the barbecue and the trailer yacht parked in front of the double cab ute.

Banks love discrete parcels of land with simple structures that are already built, that already have a certificate of code compliance and a residential resource consent embedded in the value of this ever-appreciating asset. It is money for jam with a very, very low capital requirement and an even lower risk of default.

Most banks loathe medium density housing developments with a cold, hard passion that has turned into to the phrase “bank-friendly” in the real estate ads for the exceptional apartment or townhouse that has slipped through the cracks into the mortgage book.

Banks typically don’t lend easily or cheaply to apartment and townhouse developers or the off-the-plan buyers who might fund them. New Zealand even has its own type of apartment typology specifically designed to slip through those banking approval cracks. The “dual key” apartment idea that puts a one-bedroom apartment and an adjacent studio apartment onto one title makes that one title bankable because it is more than 50 square metres, allowing the owner to rent out the sub-50 square metre studio apartment and still borrow against it.

In this week’s podcast I also talked to Kiwibank’s head of sustainability Julia Jackson about how Kiwibank is addressing these banking industry practices to try to encourage the medium density apartments that are typically more energy efficient and climate friendly.

In essence, New Zealand is not on track to meet its emissions targets for housing energy because of a range of market failures that need interventions through building codes, minimum insulation and heating requirements and an effective tax on the unaccounted-for profits on inefficient homes.

A financing and industry structure problem

This is also a financing problem that requires the state to price in the wider benefits and costs of improving our housing in its decisions about building state houses, often in a form that is cheaper in the long run and is captured in lower energy and health costs for the state at large.

But at the moment our housing industry – in which more than 70% of homes are built by small firms without the expertise, balance sheets or equipment to build complex and more energy-efficient dwelling units in larger projects – is not structured to solve this problem.

There is a lot of work to do and a lot of market failures to solve. The Climate Commission is ambitious and aspirational, but we don’t have the tools and interventions in place yet to achieve those emissions reductions drawn in grey in the chart above.

Follow When the Facts Change on Apple Podcasts, Spotify or your favourite podcast provider.