This month, Kiwibank reset its variable interest rates by 1%, from 4.40 to 3.40%. Kiwibank’s general manager of business banking Nigel Gaudin tells The Spinoff why this is a big deal for local businesses.

Okay, what is a variable interest rate? And what have you done to it?

A variable interest rate, sometimes called a floating interest rate, is a rate that changes with the market. It can go up and go down. It’s the opposite of a fixed interest rate that provides you with certainty over a period of time but gives you little flexibility.

The most common form of variable interest debt facility for business customers is an overdraft. Reducing our variable interest rate by 1% therefore reduces the rate a customer pays when they use their overdraft. As we look to the next 12 months and beyond that reduction will really make a big difference for small and medium-sized business owners.

With a variable rate loan, you also have the flexibility to increase regular payments or make lump sum repayments of any size without penalty or cost. If interest rates go down, you can pay off your loan faster by keeping your repayments at the same level. But by the same token if interest rates go up you’ll need to increase your repayments.

Why are you doing this now?

We’ve done it for two reasons. First, New Zealand is recovering from a pandemic and businesses need our help. This move gives Kiwibank customers greater flexibility, choice and savings. It provides an opportunity for our customers to pay back their loans faster, save, or buy local and support New Zealand’s economy.

Second, historically in New Zealand variable rates have been higher than fixed rates. Since the global financial crisis, the gap between variable interest rates and fixed interest rates has widened to the point where variable rates are now 2-3% higher than fixed. We want to put a line in the sand, be true to our purpose and make an impact, be the challenger that the rest of the market chooses to follow and, if they can’t or won’t follow us, it continues to further differentiate us.

What does the variable interest rate reduction mean for businesses?

Bringing the variable and fixed rates closer gives our business banking customers options. When we have a variable rate of 6% and a fixed of 3%, everyone’s going to go fixed. And the problem with fixing rates is it attracts break costs if things change, and as a business owner, you want to maintain flexibility. So if I want to sell my property, I have to break the loan I took to buy it and that costs money.

But with a variable rate, you can pay back the loan tomorrow, next month, next year, it doesn’t matter. This gives businesses the opportunity to pay off debt faster, or the flexibility to cover the costs of keeping on their employees or investing in new equipment to adapt to the new environment we find ourselves in.

What do you hope comes of this?

This is not a ‘special deal’ or a limited time offer. It’s all about doing the right thing at this moment and supporting our customers. Of course, we are hopeful this will encourage some new customers to make the switch to a great Kiwi bank and recognise that there is choice in the banking market.

Some commentators are saying we have set the cat among the pigeons. That’s probably right, and we don’t mind that one bit. Our founding vision was about being a bank that could challenge the big Australian-owned banks and back Kiwis to succeed. We’re not afraid to lead the market so we can support more New Zealanders. Now, more than ever, businesses are stepping up and doing their bit. Kiwibank is proud to play its part.

How can local businesses maximise the opportunity of lower variable interest rates?

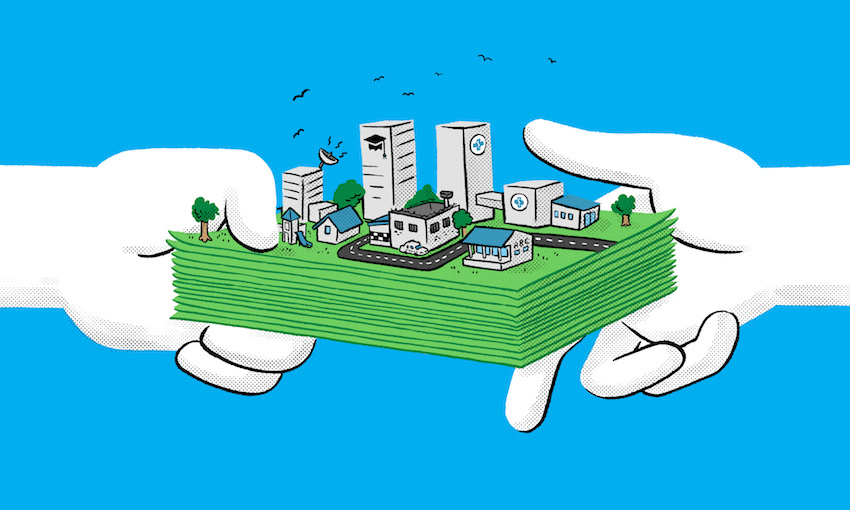

It is an economic stimulator that can be used in any number of ways. Business A might take the leap and buy that extra piece of equipment they need. Business B might keep their staff employed. Business C might just keep its doors open. Lowering the interest rate puts money in businesses’ pockets. What they do with that is up to them.

All businesses need to be financially sustainable and our strategy is to grow. This is about delivering on our purpose to make Kiwis better off and it is this that will ultimately benefit both Kiwibank and New Zealand.

What’s the benefit to Kiwibank customers?

Somewhere around $20 million in interest savings over the next 12 months. But we want to really put a line in the sand and say to our competitors, ‘come with us, and do the right thing for New Zealanders’. If other banks follow us the contribution to New Zealand could be hundreds of millions. So if we can lead the way, why not? Why wouldn’t we?

Every business that can help, should help. And every business that needs help should get as much help as they can. As larger companies, we’ve got a big role to play in New Zealand’s recovery. This is part of our contribution.

This content was created in paid partnership with Kiwibank. Learn more about our partnerships here.