When we think about assets, often those are houses, cars and large investments. But for most of us, our biggest asset is actually our earning potential. So what if we suddenly can’t work?

This content was created in partnership with Kiwibank.

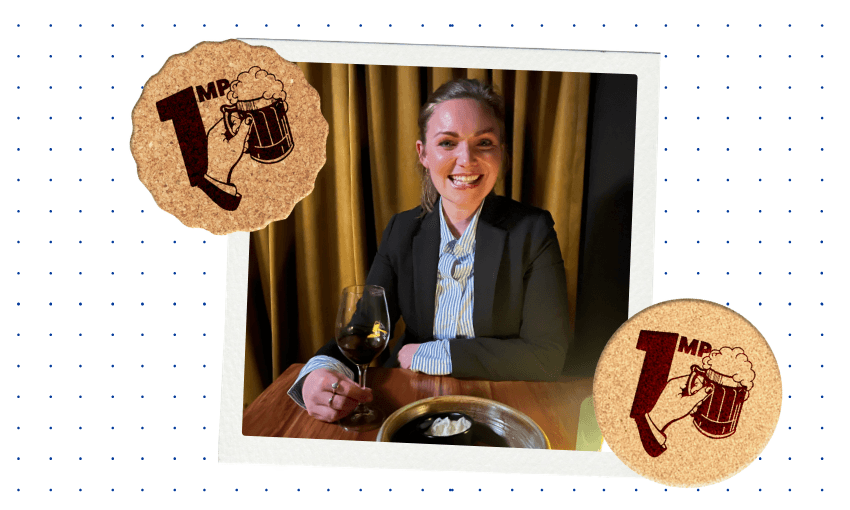

When Susan* turned 45 in 2016, booking in for a mammogram wasn’t at the top of her birthday list. But when a colleague at work was diagnosed with breast cancer, she was reminded about free biennial breast screening for people 45 and over, so just to be safe she booked in, went for a check-up and was told results would take a couple of weeks.

Two weeks later she got a call from the clinic. “I was fully expecting to hear ‘it’s all good we’ll see you in two years’, but they didn’t say that. They said they needed to do another mammogram and there were some things they needed to check,” says Susan. She went back and biopsies confirmed the worst: she had breast cancer.

For most of 2017, she received various forms of treatment. She was unable to stay working and struggled to be the energetic mum her two kids were used to. “I lost a year of my life to getting through treatment and recovering from it,” she says.

“One of the things that going through all the chemo made difficult was the impact on my kids and not being able to be the mum that they knew. I didn’t have the energy to go out and play with them – I could sit on the couch and that was about it.”

While the implications of being out of work for so long could have been significant, Susan’s trauma insurance helped to ease financial stress – meaning she was able to focus fully on recovery, without the implications of her family going from two incomes down to one.

“If you don’t have that financial pressure, it really does lessen the impact of the situation that you’re in. I don’t even want to think about what it would have been like if we didn’t have insurance. It took the stress away,” she says.

“The trauma insurance payout gave me breathing space to go back to work when I felt like I could actually cope, rather than going back too early and only managing a couple of hours of work before having to go to bed for the rest of the day.”

Most New Zealanders wouldn’t have savings to fall back on if things went wrong for an extended period of time. The latest figures from Stats NZ show that as a nation, we’re spending almost all of our earnings. For the year ending March 2020, each New Zealander was left with only $412 annually on average after their outgoings. Saving money isn’t the norm.

That $412 wouldn’t go far if a person suddenly found themselves out of work due to illness or injury. Serious Illness Trauma cover and Income Protection Illness cover are insurance options available as part of Life & Living Insurance, which gives people peace of mind about their income should serious illness or injury occur.

Illness isn’t inevitable, but it’s certainly not rare. More than one in 23 New Zealand adults have been diagnosed with heart disease, more than 38% of us will be diagnosed with cancer before the age of 75 (up from 28% in 2012), and every 45 minutes a New Zealander suffers a stroke.

All these types of illnesses have the potential to stop someone from working for months, if not years. But with Life & Living Insurance, Income Protection Illness cover can pay a monthly amount of up to 55% of normal income to ease some of that stress. Serious Illness Trauma cover can also pay a lump sum if you’re diagnosed with a defined medical condition, such as severe cancer or severe heart attack.

Insurance isn’t a permanent solution to money woes, but it offers a temporary safety net that can alleviate at least some of the emotional and financial distress that is often interwoven with illness and, for loved ones left behind, death.

For parents, homeowners and those with additional assets, life and living insurance may have been on the radar already, but contrary to common belief, life and living insurance isn’t just for people who fit these demographics.

Whether that be paying rent, buying groceries, or continuing normal leisure activities, life and living insurance can help ensure that without employment, the claimant can still maintain some pillars of their normal life.

Kauen Nauer, Kiwibank’s regional manager for Auckland North, says one reason people decide to not take out Life & Living Insurance is because they feel owning a house is enough security.

“A lot of people talk to me about their back-up plan being selling their property,” he says. “But selling up is one of the worst things you can do when you’re going through a traumatic or challenging life event. I think people look at it as a transactional event but it’s so much more than that.”

For people who are hopeful of owning a home one day, Nauer recommends insurance sooner rather than later. “One of the things I always talk to people about is if their dream and goal is home ownership, then why wouldn’t they have insurance now? If something was to come along and stop them from being able to work and save for a deposit, how hard would that make saving?” he says. “But if you had a plan in place and had insurance, at least there’s still something that’s going to help achieve that goal.”

For New Zealanders unfamiliar with insurance it can be difficult to know what cover to get. We all have different incomes, different outgoings and different comfort levels around risk.

Kiwibank’s online estimator tool helps to give people guidance about the right cover for their situation, taking into account things like financial dependents, current savings and debts.

It’s common to insure your car, your contents and your home, but there are so many other insurance options to cover assets that may not be as obvious; like your ability to earn, your health and lifestyle.

“It’s about having the right conversation with people and finding out what’s important for them to have covered,” says Nauer.

Put simply, life and living insurance can provide options and time to recover. For Susan, it gave her the ability to recover for more than a year without needing to jump back into work when she wasn’t ready.

“You do think things happen to other people, but sometimes they don’t and they happen to you,” she says. “What would you do if the thing that happened to other people did happen to you? How would you manage?”

*First name used to protect anonymity.

This content was created in partnership with Kiwibank.

Follow When the Facts Change, Bernard Hickey’s essential weekly guide to the intersection of economics, politics and business on Apple Podcasts, Spotify or your favourite podcast provider.