Bitcoin has experienced an unprecedented explosion in value over the past eight years. Here Richard Meadows outlines just what it is, and why the good times won’t last.

In the winter of 1928, Joe Kennedy stopped to get his wingtips buffed on his way to the office. After the shoeshine boy finished, he offered the businessman an unprompted stock tip. Kennedy mulled this encounter over, then sold off his entire portfolio, just in time to avoid the carnage of the Great Depression.

Right now, the whispers on the street are all about bitcoin, along with the slew of similar ‘cryptocurrencies’ inspired by its tremendous success. Bitcoin is up 500 per cent this year alone, minting new millionaires from those who have ridden the stratospheric boom.

When shoeshine boys are giving out stock tips, you know it’s probably time to get out of the market. With that in mind, let me present my candidates for the Four Horsemen of the Cryptocurrency Apocalypse:

- A claim that an Auckland high school is cracking down on kids using the school WiFi to access Bitcoin sites.

- Burger King launches its own version of bitcoin in Russia, called the WhopperCoin.

- A pensioner looking to preserve her carefully saved nest egg asks me if she should transfer it all into cryptocurrencies, because she isn’t sure about the safety of the bank.

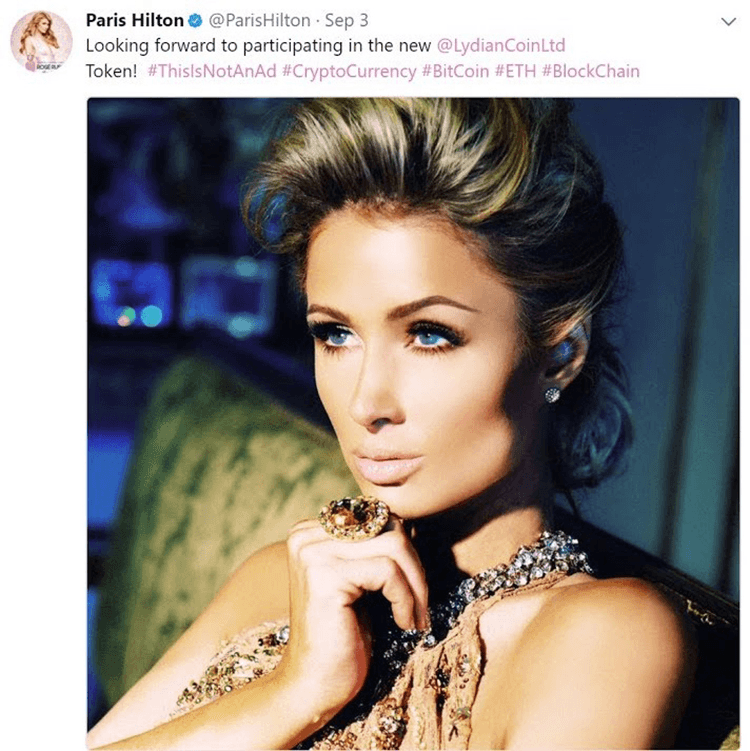

- Famously famous person Paris Hilton climbs aboard the #CryptoCurrency bandwagon, later deleting her tweets after the eyebrow-raising new coin is embroiled in controversy.

Could these be harbingers of the Judgment Day that is surely coming?

Amongst the crypto-fever afflicted, these sort of warnings hold about as much interest as a ragged bum on the street corner, proclaiming that the end of the world is nigh. Their gaze glides right on by, quickly returning to the transfixing zeroes and ones dancing before their eyes.

And fair enough, too. It’s hard to even comprehend the staggering return on investment earned by those who have ignored naysayers and held the faith. The first recorded purchase on the Bitcoin network, in 2010, involved the exchange of 10,000 bitcoins for a couple of pizzas. Today those coins are worth $84 million, which means that guy bought the most expensive pizza in the history of the universe (you have to hope he at least got stuffed crust).

Anonymous digital money has long been a tantalising idea for libertarians, but it wasn’t until the early noughties that decades of improvements in cryptography and computer science made it possible. In 2008, a paper authored by someone calling themselves Satoshi Nakamoto outlined a way to make the fantasy a reality – a purely digital currency that would let people privately send money to anyone in the world, that was completely decentralised, free from interference from governments and other third parties, and secured by ingenious collaborative cryptography. And so, Bitcoin was born.

To this day, no-one knows who Nakamoto is. The shadowy founder and Ayn Randian underpinnings didn’t exactly inspire confidence, and for a long time, bitcoin was mostly ignored as the nefarious plaything of hackers and drug dealers doing shady shit on the dark web.

While the stereotype was geeky teenagers buying weed online, the real vision was much, much grander: To vastly reduce transaction costs, not just for rich tech-bros, but for the ‘unbanked’ poor and migrant workers currently charged rapacious remittance fees to send their meagre earnings home. To make credit card fraud a thing of the past. To create self-executing ‘smart contracts’ between total strangers, without meathead humans messing things up. To finally enable cost-effective micropayments for content producers and activists. To shrug off the vampiric layer of banks and financiers with their insatiable mouthpieces latched onto everything, as well as the fickle bureaucrats, central bankers and politicians who can change the value of your coloured pieces of paper at their will. An entirely new system of commerce, by the people, for the people.

If you’re wondering how you missed this techno-utopia springing up around you, well, it hasn’t really happened yet. Transaction volumes are pretty measly, and hardly anyone actually uses bitcoin to buy and sell stuff – they’re too busy hoarding them all. No-one wants to be the guy who accidentally buys a million dollar pizza.

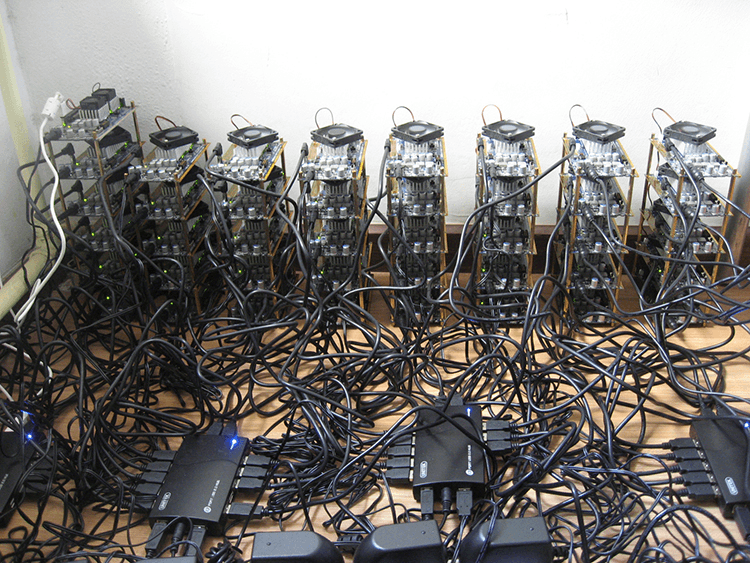

New bitcoins are created roughly every 10 minutes, but the process is getting harder and harder, with the supply programmed to tap out by 2140. The spoils go to ‘miners’, who devote computer resources and electricity to running mathematical problems that check the validity of transactions and create new ‘blocks’ in the chain.

What the miners are really doing is record-keeping on a scale never seen before: A giant public ledger, stored on millions of computers around the world. It contains every transaction in history, going right back to the very first ‘Genesis’ block, but the whole file could still fit on your old iPod. Every time someone wants to transfer bitcoins, miners check the ledger to see if the sender actually has the money. Like an insect in amber, the successful transaction is preserved for time immemorial, coated in thicker and thicker layers of cryptography which make it increasingly difficult to hack.

The more people who participate in the system, the better for everyone involved. One way of describing this situation is a ‘positive feedback loop’. Another way of describing it is a ‘big fat bubble’.

Bitcoin has no intrinsic value whatsoever. It’s not pegged to any other currency or commodity. It doesn’t carry a guarantee or backing from anyone. It pays no dividends, and grows no wheat.

Instead, its value is whatever the market says it is. That makes it a purely speculative play, and highly volatile – it’s already been through a mini-bust in 2013. While the price has soared over the last year, it hasn’t exactly been a smooth ride:

The only way anyone buying bitcoin can make money is by hoping someone else will pay even more for it tomorrow.

This is concerning, because the hoarders have a massive vested interest in luring in greater and greater fools to keep the bubble from bursting. There are no scruples in Crypto-land, which is infamous for outlandish claims – my personal favourite being bitcoin advocate John McAfee’s promise to “eat his own dick on national television” if the price doesn’t reach $US500,000 within three years.

The more glaring problem is the legion of Bitcoin copycats and alternative coins, which already number over 900 and counting. Jordan Belfort, better known as The Wolf of Wall Street, has described these initial coin offerings (ICOs) as “the biggest scam ever” and “far worse than anything I was ever doing”. When the voice of reason is a fraudster who used to fall asleep on piles of cocaine big enough to use as a pillow, something is probably wrong.

Companies have realised they can raise vast sums of money by conjuring a new currency out of thin air, then selling it to unsophisticated investors who froth their tits over anything vaguely related to crypto. The valuations are out of this world – companies crossing the billion-dollar mark with a handful of staff, and products that don’t even exist yet. While some of these businesses are doing genuinely interesting things, plenty are blatant ‘pump-and-dump’ schemes. ICOs are usually conducted without jumping through the normal regulatory hoops, which has led to predictably farcical situations.

We live in a world where Dogecoin, a deliberately satirical coin based on a meme, was not long ago valued at US$400m. That’s not even close to plumbing the depths of the people playin silly buggers. For sheer brazenness, it’s hard to look past Useless Coin, which billed itself as “the world’s first 100% honest Ethereum ICO. No value, no security, and no product. Just me, spending your money.” (Note that it still managed to take US$91,000 from investors).

This looks a lot like the dot-com boom all over again. In the late 90s, everyone lost their minds about this amazing new ‘world wide web’ thing. Investors tossed money hand over fist into buying any stocks with a cool-sounding name, ignoring the boring old financial metrics of days gone by. This exuberance became a self-fulfilling prophecy which worked brilliantly as an investment strategy – right up until it didn’t.

The Internet was such a wildly exciting and transformative technology that everyone decided the usual rules didn’t apply. In 2017, blockchain and crypto hawks are making the exact same claim. Predicting the future is a dangerous business, but let’s note that every bubble spanning the last eight centuries has been ramped up by people insisting that ‘this time is different’. Every single time, they’ve been wrong.

At some point, the grown-ups are going to take the punch bowl away. There’s no way any of these outrageous claims and non-disclosures would fly, if it weren’t for crypto floating in a weird sort of grey area between geographies and existing securities laws. Regulators haven’t figured out how to handle it yet, but they’re definitely taking a keen interest.

Last week the Financial Markets Authority laid out its compliance expectations for any NZ-based ICOs, and posted some general words of caution for investors. In the US, the Securities and Exchange Commission (SEC) has warned that some ICOs may be classified as securities, and therefore subject to regulation, and also taken action against the most obviously fraudulent schemes. China and South Korea have banned ICOs altogether, and it’s possible that Japan will follow suit.

The longer the world’s regulators sit on their hands, the higher the potential body count grows. While this is going to cause a lot of hurt for a lot of people, the boom and (impending) bust of the ICO bubble is sort of a good thing. The speculative period during the early adoption period of new technologies helps attract a flood of capital, with at least some of the profits reinvested in the platform. Greed is the perfect vector for raising awareness, with a wave of FOMO rippling through society until even your grandma is sending you texts about the price of Ether.

The dot-com boom was one of the biggest bubbles in history, but that didn’t mean the web was not, in fact, a huge deal. Today’s titans of industry – Google, Facebook, Amazon, The Spinoff – are mostly digital companies, and we couldn’t imagine life without the Internet. The hype was real, but there had to be a big painful consolidation before we could unlock the real potential.

The same is true of crypto. The financial system is long overdue for an overhaul, and people are right to be excited about that. It wouldn’t be surprising if some application of blockchain technology became as ubiquitous as the personal computer and the Internet, both of which were originally pooh-poohed by sneering critics who failed to see the writing on the wall.

Right now, the froth and the fury is all-consuming. Eventually, the attention and money will refocus in more productive places – i.e, the actual use cases of the technology – but not before the unpleasant task of lancing the boil.

Perhaps, unlike tulip bulbs, canal mania, railways, the roaring 20s, penny stocks, the US housing bubble, the dot-com boom, and every other sudden explosion of asset prices in history, this time really is different.

If so, I promise I’ll do the honorable thing: which is to say, tuck in a napkin, fetch the Tabasco sauce, and eat my own dick on national TV.

The Spinoff’s business content is brought to you by our friends at Kiwibank. Kiwibank backs small to medium businesses, social enterprises and Kiwis who innovate to make good things happen.

Check out how Kiwibank can help your business take the next step.