The German men who tried to market pink gloves for handling tampons show how highly male inventors are valued over their female counterparts – no matter how ridiculous their ideas, writes Jessica C Lai.

“It’s a man’s world” is true across many contexts, including the created world we encounter daily – the world of buildings and things. This is because it is men who have historically been able to successfully commercialise their inventions. It is their ideas that get get the lion’s share of funding and legal support and construct the world we live in.

Why is it that men get more entrepreneurial funding than women? The answer to this is complicated. But it is in large part due to hundreds of years of men being public figures of industry while women took care of the private sphere. As a result, most venture capitalists are men and they tend to associate market-worthy inventions with male inventors. The archetype of the entrepreneur, the start-up genius or the market-savvy inventor is a man. In contrast, women are commonly viewed as too emotional, irrational and lacking in entrepreneur ability.

With more funding, men are more likely to be successful in bringing their products to market. Just as important can be protecting one’s invention with intellectual property. Studies show having a patent – which protect technical inventions with up to 20 years of exclusive rights – can increase the chances of getting venture capital. Exclusive rights can also reduce market competition, which increases the likelihood of success.

Yet, worldwide, women make up less than 15% of inventors named on patents. Part of this is attributable to the way patent offices treat women inventors and inventions made for women.

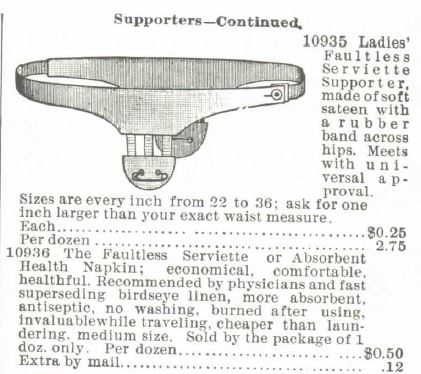

To illustrate, in the second half of the 19th century, the US patent office described a women’s safety belt, designed to hold sanitary napkins in place, as “necessarily somewhat trifling”. In the same period, the US patent office enthusiastically pronounced that a minor improvement for men’s undergarment was “graceful”, “making not only a genteel, but comfortable fitting garment” and “a very great improvement”.

You might be thinking, “Well, that was the 19th century. Since then, we’ve given women the right to vote. We’ve had the feminist movement. There are more women in science. The prime minster of New Zealand is a woman. What more do you want?” You might even be thinking, “Calm down, you angry feminist.”

But I am an angry feminist who is not going to calm down, because – despite the feminist movement and women in positions traditionally representing power – in many ways nothing has changed. Equal rights do not mean equal opportunity or that misogyny has somehow evaporated into the ether. So we should all be angry feminists.

Let’s look at a current example that shows how bias remains in the way inventors and inventions are viewed, despite equal rights and women in power. We’ll turn to Germany, where Angela Merkel has been chancellor since 2005. Germany has had 16 years of seeing a woman as the leader of one of the world’s strongest economies and an indomitable figure on the European and global stage. In 2020, the World Economic Forum ranked Germany as having the 10th narrowest gender gap in the world (New Zealand ranked sixth).

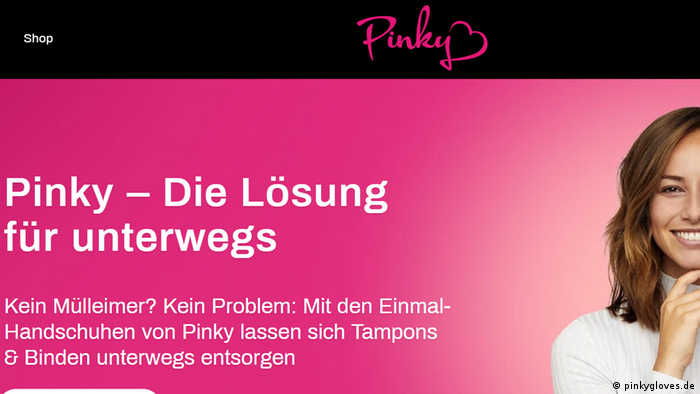

Yet, just this month, two men presented their “innovative” idea on the German version of The Lions’ Den, Die Höhle der Löwen, seeking investor money for “Pinky Glove”. Their product was literally pink gloves, which women could use to remove, package and conceal used sanitary napkins and tampons.

The men said they came up with the idea after living with women and being disgusted at seeing their used products in the bin. This prompted them to create an opaque and sanitary means of hiding away any evidence of periods. One of the “lions”, a prominent German businessman, decided to invest €30,000 (NZ$50,000) in the product.

There are many issues to unpack here – too many for the confines of this article. First there’s the fact that men are trying to sell a product to women that women do not need and which is unsustainable. More sinister is that women are being told they need to make private something that is natural and biological, because society casts menstruating people as unclean and impure. But, never fear, here come men willing to sell them the cleanliness and purity they clearly so desperately need.

In 2019, Kati Ernst and Kristine Zeller were on that same show, Die Höhle der Löwen, seeking funding for menstrual underwear, “Ooia”. This was something women wanted – a product made by women for women. It was also something far more sustainable than disposable products. Yet they did not get any funding from the show.

This is sadly unsurprising, as women are not perceived as entrepreneurs. And why would men support a product that normalised periods, bringing them into the light of the public sphere, embodied in unashamedly attractive underwear?

Now you might be thinking, “Well, surely this wouldn’t happen in New Zealand.” But even as I write, Stuff has just reported that Facebook and LinkedIn pulled an advertisement for Vitals, a Kiwi company making period underwear, on the basis of “inappropriate or offensive language” and “sexual related content”.

So instead of supporting women who create inventions for women, and instead of normalising something normal, we continue to shame more than half the population for having periods and we make them pay for that shame.

At €11.96 (NZ$20) for a pack of 48 Pinky Gloves, the company was hoping that women would pay yet another “tax” for having a uterus. That’s on top of the cost of sanitary products, which most women are forced to regularly buy.

Attempts have been made in New Zealand to negate this women’s tax. In 2016, Pharmac was petitioned to subsidise tampons and pads. Pharmac is the government agency with the objective “to secure for eligible people in need of pharmaceuticals the best health outcomes that are reasonably achievable from pharmaceutical treatment and from within the amount of funding provided”. Pharmaceuticals are defined as medicines, therapeutic medical device, or related products or things.

Pharmac declined the funding application on the basis that “sanitary products are not medicines or medical devices”. Pharmac further stated there was insufficient information to show sanitary products helped address a health need. After all, menstruation was a “normal bodily function” and not a “health need”.

This distinction is hard to accept, especially when one notes Pharmac does fund incontinence pads and pants, as well as paediatric nappies. Aren’t these products often for “normal bodily functions”? Incidentally, Pharmac also funds gloves.

Nevertheless, one narrow and inconsistent interpretation later, women continue to be forced to pay this tax for having a uterus. Those who cannot afford it have to use rags and newspapers, or use tampons and pads for longer than they should, which can result in serious infections. Of course, the medicines to treat those infections could be funded by Pharmac. So why not use the funding to prevent infection in the first place?

The New Zealand government has since put money towards providing access to sanitary products in schools. But this a bandage (which are also funded by Pharmac) to a much deeper problem.

Those in power are more willing to fund that made by men and for the benefit of men. Women’s needs are invisible – as are women inventors and their inventions.

Jessica C Lai is an associate professor of commercial law in the Wellington School of Business and Government at Te Herenga Waka—Victoria University of Wellington.