What better farewell present than a fresh crop of political argy-bargy over NZ Super?

Talk about committing to the bit: last week Jane Wrightson, the retirement commissioner, retired. Or semi-retired, at least. She will remain in a number of governance roles, but is drawing the curtain on the day job.

Across four decades, Wrightson has occupied some of the top roles across a constellation of public media agencies, including the Classifications Office, the Broadcasting Standards Authority and New Zealand on Air (her thoughts on all of that are here). In 2019 she decided to take on a very different challenge.

“It was a massive change for me,” Wrightson said of her appointment as retirement commissioner. “I had run crown entities before, I knew how to do that,” said Wrightson. “And this crown entity was in a little spot of bother at the time, so needed some sorting.”

The office had been attracting unwelcome headlines, with Wrightson’s predecessor under a cloud over her leadership style. It made for a challenging inheritance. “The organisation had had a 60% staff turnover in the preceding 12 months, which meant most of the IP had walked out the door,” said Wrightson on a special episode of The Spinoff’s Gone By Lunchtime podcast. “So there was a complete reset to be done, and that’s actually work I can do. I was quite competent and confident about that. Learning about the other piece of the commissioner’s job, which is more around advocacy and policy and strategic thinking, that was the challenge, a good challenge for me.”

Moving into the financial services sector was “a huge change”, she said. That was compounded by the Covid lockdown, enforced just three weeks into the new job. “Not having the instinctive answers to what are quite basic questions to me now was just terrifying – because you really don’t want to give the wrong information out, do you?”

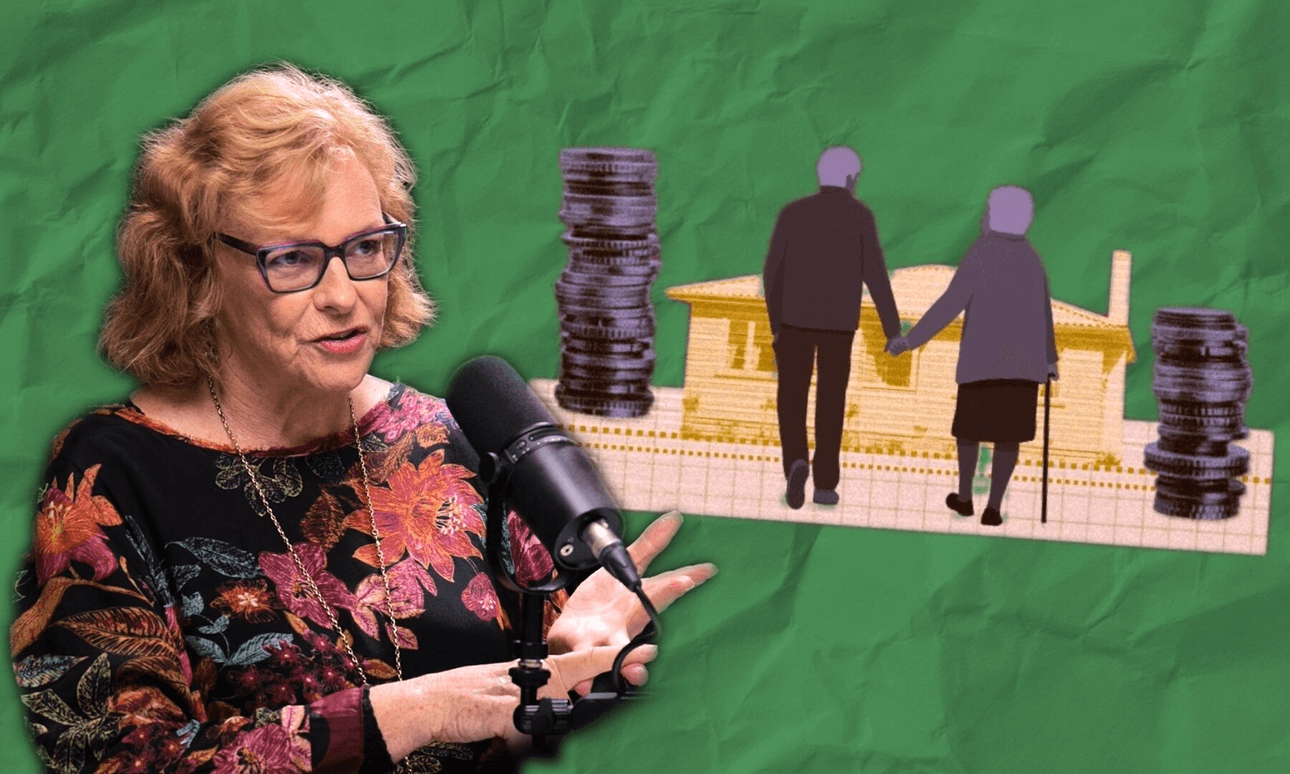

Six-and-a-half years later, the politicians of New Zealand have delivered a farewell gift in the form of fresh slings and arrows over superannuation and KiwiSaver campaign pledges. The Treasury is warning that keeping the spend on superannuation stable would mean bumping the age of eligibility up to 72 over the next 40 years.

“What I’ve tried to lay out quite carefully is that things like NZ Super and KiwiSaver are interlinked, right? It is a system. It’s a retirement income system, and you can’t really talk about change to one without change to the other, and, indeed, wider settings, like tax and other incentives that may be available. What we’re really good at is grasping one problem and going: I’ll solve that. Is it the age of superannuation? Is it whether KiwiSaver is compulsory? Is it the contribution rates? I say it’s none of these things. Collectively, it’s an issue the country has to address. And collectively, you would hope the politicians, once they finish doing their electioneering – which is, you know, the democratic process – you would hope that we could find a way for at least the major parties to start talking together and going: what is the 10- to 15-year solution for New Zealand that will take into account all the issues around this?”

The reality, she said, was that bumping up the age of superannuation might be fine for many people, but not all. “It doesn’t solve a whole bunch of other problems. How are you going to mitigate the impact on women, or Māori and Pasifika, manual workers?… Women’s retirement savings are, generally speaking, 25% less than men’s – the gender pay gap turns into the retirement savings gap. So you’ve got some systemic things to think about. It’s a bit like infrastructure, right? We can’t do this on a three-year cycle with kneejerk reactions.”

As to whether NZ Super is sustainable as it is, “well, it depends who you ask”, said Wrightson. “The economists will generally say no. The flipside to that is we’re around about the middle of the OECD. It costs about five-point-something-percent of GDP at the moment, predicted to go up to six, so we’re still in the middle. We’re neither bad nor good.” The challenge was to “encourage a savings mentality when we have a large low-paid workforce and an increasing gig economy? Hard stuff”.

While the Australian system, with its compulsory, employer-funded superannuation, was often gazed at with envy, that was costing plenty, said Wrightson. “There’s a 12% employer contribution that’s funded by tax breaks. And the size of those tax breaks are astronomical – not far off the entire cost of NZ Super, and when it’s a workplace-saving scheme that mirrors the inequities of the workforce, right? NZ Super is a gender-blind universal basic income, so fairer. All of these things have to be thought about. I don’t think it’s too much to ask our politicians to go wider than one idea.”

She does have one standalone idea, however: “I’d quite like to call it something else, like KiwiRetirement, because it’s [currently] not seen as a retirement fund as much as a savings account. So people are saying, ‘it’s my money. Give it to me.’ And you’re going, ‘No! You can’t do it in Australia. You can’t do that anywhere else. It’s your retirement fund. If you want to save for other things, then minimise your KiwiSaver and maximise your other savings pot.”

Wrightson was surprised by the scale of another challenge: debates between operators and advocates for residents of retirement villages. “I walked in and saw, in effect, two types of people vigorously arguing, not listening to each other, and no kind of principled approach for solving the problem… So I said, what are the core problems here? And it was very hard to understand. So we published a white paper… we got 3,000 responses, which is slightly staggering and published a response asking the government to look at reviewing the legislation. The legislation is more than 20 years old now… and it was very heavily weighted in favour of the operators.”

Fresh legislation that covers, for example, the terms by which operators must repay residents or families for vacated properties, will soon go before parliament.

As she begins her own post-full-time employment, did Wrightson’s discoveries in the retirement commissioner’s chair inform the way she herself wanted to retire? “In part,” she said. “I mean, you don’t really think about it until it becomes disturbingly close. The first thing you ask is, do I want another three years, and then what would that look like? And then what would be the trade-offs and the alternatives? I thought, I don’t think I want to work full-time in an executive or chair role any more. I think I want to do more portfolio work, and I think I want to step down gradually. And that’s what this job has taught me, that the people who jump off the cliff from full-time work to nothing often really flounder, because the lack of structure in your day is quite challenging. So I’m, you know, doing the step-ladder.”