Right now New Zealand’s banks could easily double mortgage debt and borrowers, on average, could easily afford it. In an already overheated housing market that might lead to disaster, writes Bernard Hickey.

Subscribe to When the Facts Change on Apple Podcasts, Spotify or your favourite podcast provider.

The banks of this country present themselves as safe, competent and sensible corporate entities that serve the best interests of their customers, shareholders, staff and society alike. That’s broadly true now, but it’s not the natural or inevitable state for banks generally, and it hasn’t always been the case here.

Banks are special and deserve to be treated as such by the government and the Reserve Bank. Alone among other corporate entities, banks have the power to create money. This is still a controversial and uncommon thing to say, but it’s true, as the Bank of England reminded everyone seven years ago in this seminal paper, ‘Money creation in the modern economy’.

“Money creation in practice differs from some popular misconceptions — banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they ‘multiply up’ central bank money to create new loans and deposits,” Michael McLeay, Amar Radia and Ryland Thomas of the Bank’s Monetary Analysis Directorate wrote in the paper.

This surprisingly accessible 27 pages of financial heresy from the world’s most powerful central bank (at least until the creation of the US Federal Reserve in 1913) caused a sensation when it was published in early 2014. Essentially, it was the head magician revealing the tricks behind the “magic” of where money came from in the modern era of globalised capital flows, fractional reserve banking and “fiat” money, which is where a nation’s currency is not backed or tied to a gold standard or another currency.

“Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money,” central bankers wrote in bold.

They were quick to point out banks couldn’t just go around willy nilly creating money and pumping huge amounts of cash into the economy and asset prices because the central bank effectively set short term interest rates to ensure the money supply didn’t grow too fast as to fire up inflation, or too slow as to create deflation. Also, the central bankers reassured readers, regulators forced banks to hold a certain amount of shareholder’s capital and liquid assets in reserve to ensure any bank could handle a surge of deposit withdrawals or losses from bad loans, which could happen in tandem if savers lost confidence in a bank. They’re referring to rules that banks must have about 10% of their own shareholder equity behind their loans and a certain portion of their funding must be held in a very stable and long-term form, to reduce the risk of a “run”.

I quote the paper in full and with the bolding included to emphasise the point for those, including many I encounter in banking and economics, who argue that banks have the same constraints and practices of other firms. Banks, they argue, are just like any other company buying things and then selling them with the hope of making a profit. Banks, they argue, are not that special or important, and therefore they shouldn’t be ‘interfered’ with by governments and regulated as if they are bombs just waiting to blow up. You could feel the barely suppressed fury of some commentators in recent weeks as they raged about the loss of independence of the Reserve Bank and the interference with the operations of private companies.

The truth is banks can be dangerous and enormously powerful in an economic and societal sense, and mostly not in a good way. Up until the advent of proper bank regulation and more active central banks in the late 1930s, there were regular banking crises, financial booms and wild swings between banks lending too much, and then collapsing in a heap. Often these crises and collapses went on to generate depressions.

The Chicago Plan of 1936

Banking collapses in Europe and the United States caused the Great Depression of the 1930s that forced western governments and thinkers, and America in particular, to look at regulating banks as if they were timebombs, and to intervene much more aggressively when financial instability threatened the real economy. These were the lessons taken in 2008/09 and in March last year.

Yale University economics professor Irving Fisher and University of Chicago economics professor Henry Simons proposed in 1936 that banks should have 100% of their own shareholder capital in the form of retained earnings behind their loans, not the 5-10% that has been typical over the last 100 years or so. They proposed that all bank deposits be backed by government-created money held in reserve, rather than less accessible and reliable deposits and bonds.

The idea was that these reforms would substantially reduce the chances of further depressions and take of lot of volatility out of the economy and asset prices. Fisher and Simons argued that recreating a new safer banking system was much more possible when the system was in crisis and mostly broken. It’s worth remembering that president Franklin Roosevelt closed the entire US banking system for a week in March 1933 after a month-long banking run so he and Congress could invent a government deposit insurance scheme and start restructuring and rescuing banks. It worked, as the Federal Reserve Bank of New York wrote in 2009. For good measure, Roosevelt then ordered all Americans to sell almost all their gold back to the US Federal Reserve for US$20.67/oz (about US$400/oz in today’s money). He then changed the rate of exchange to US$35/oz overnight, effectively devaluing the US dollar by almost half. Eventually the US dollar was taken off the gold standard entirely.

This 1936 Chicago Plan was revisited by the International Monetary Fund (IMF) in 2012 in this paper, which looked fondly back on the idea as a big missed opportunity. Again, I’ll quote in full from the IMF’s Jaromir Benes and Michael Kumhof to show how bomb-like unregulated banks had become, and how they have become central to modern economies:

“Fisher claimed four major advantages for this plan:

First, preventing banks from creating their own funds during credit booms, and then destroying these funds during subsequent contractions, would allow for a much better control of credit cycles, which were perceived to be the major source of business cycle fluctuations.

Second, 100% reserve backing would completely eliminate bank runs.

Third, allowing the government to issue money directly at zero interest, rather than borrowing that same money from banks at interest, would lead to a reduction in the interest burden on government finances and to a dramatic reduction of (net) government debt, given that irredeemable government-issued money represents equity in the commonwealth rather than debt.

Fourth, given that money creation would no longer require the simultaneous creation of mostly private debts on bank balance sheets, the economy could see a dramatic reduction not only of government debt but also of private debt levels.”

Just let that sink in for a bit. Changing the way banks were able to leverage up their equity in a virtually unlimited way and forcing banks to always have money in reserve for all deposits would have removed debt from the modern economy, both public and private debt, and stopped bank runs and collapses.

The Chicago Plan was never implemented because the banks and the global economy was beginning to recover by the end of the 1930s (for obviously ominous reasons) and the moment to rebuild from the rubble had passed.

Learning the lessons of history

But the banking collapses of the Great Depression and Chicago Plan became suddenly topical again in the wake of the global financial crises of 2007 and 2008 and the European debt crises of 2010, 2011 and 2012. Hence the IMF paper, and the subsequent Bank of England paper. These debates about how to tame the wild instincts of banks with fractional reserves in “fiat” money systems led to increases in capital requirements for banks and much tougher rules about the way banks funded their loans and kept money in reserve.

Even in New Zealand

That happened in New Zealand too. The Reserve Bank, which acts as both bank regulator and monetary policy manager (unlike in most developed economies which have separate bank regulators), imposed an increasingly tough ‘core funding ratio’ from 2010 to 2013 that meant banks had to have funding that was long-term and stable, either in the form of longer-term bonds or retail term deposits. That removed the risk of short term money markets in New York and London freezing, as they did in late 2008 and early 2009. New Zealand’s big four banks were reliant at the time on 90-day bank bills that could be pulled in a crisis. That’s what happened in early 2009, forcing the Reserve Bank to quietly lend $9b to New Zealand’s banks through a ‘term auction facility’ to ensure those 90-day bills could be repaid. It was an extraordinary intervention by the government to effectively help the big four banks and it worked, as the Reserve Bank quietly documented in this June 2011 paper.

That’s why the Reserve Bank, especially under Adrian Orr since 2018, has also been trying to force the banks to increase the amount of capital they hold from around 10% to closer to 20%. The Reserve Bank suspended that increase when Covid struck, and also lowered its core funding ratio requirement from 75% to 50%. These changes were little noticed alongside the much more prominent concession to the banks and the economy of removing the loan to value (LVR) restrictions that had been place since late 2013.

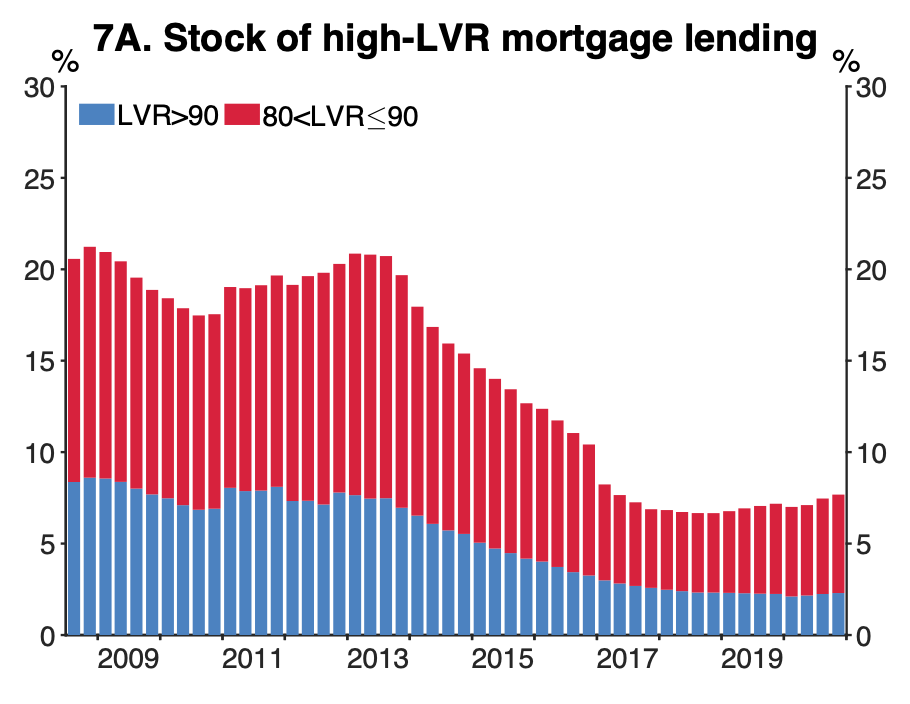

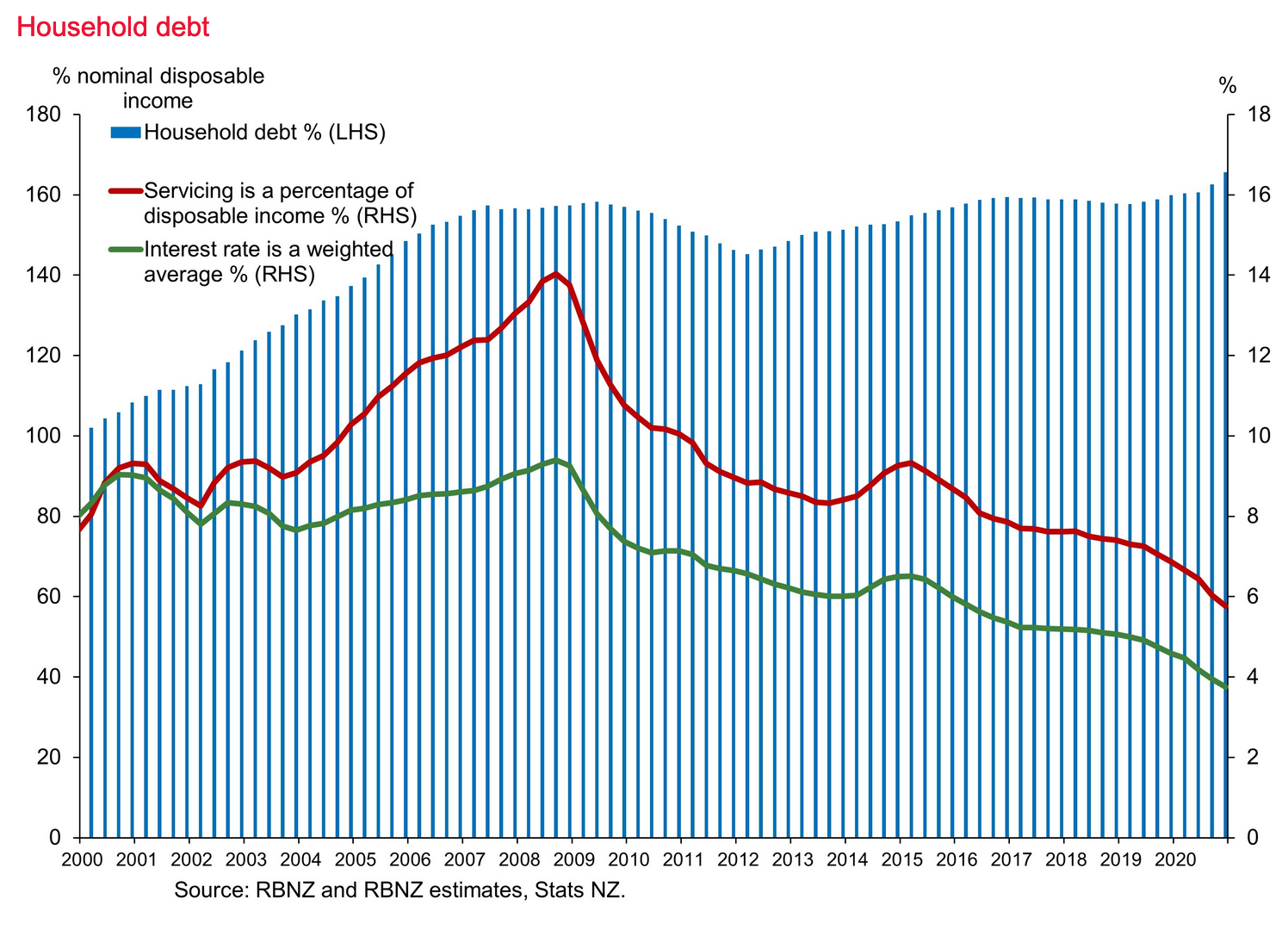

The Reserve Bank, under previous governor Graeme Wheeler, introduced the restrictions and then tightened them under the increasingly uncomfortable noses of then prime minister John Key and finance minister Bill English from 2013 to 2017. Wheeler did it because he could see how the banks would pump enormous amounts more debt into housing valuations without those restrictions, particularly as interest rates kept falling ever lower for ever longer. This chart shows how effective it was in reducing the risks in New Zealand’s mortgage book.

When the shackles came off

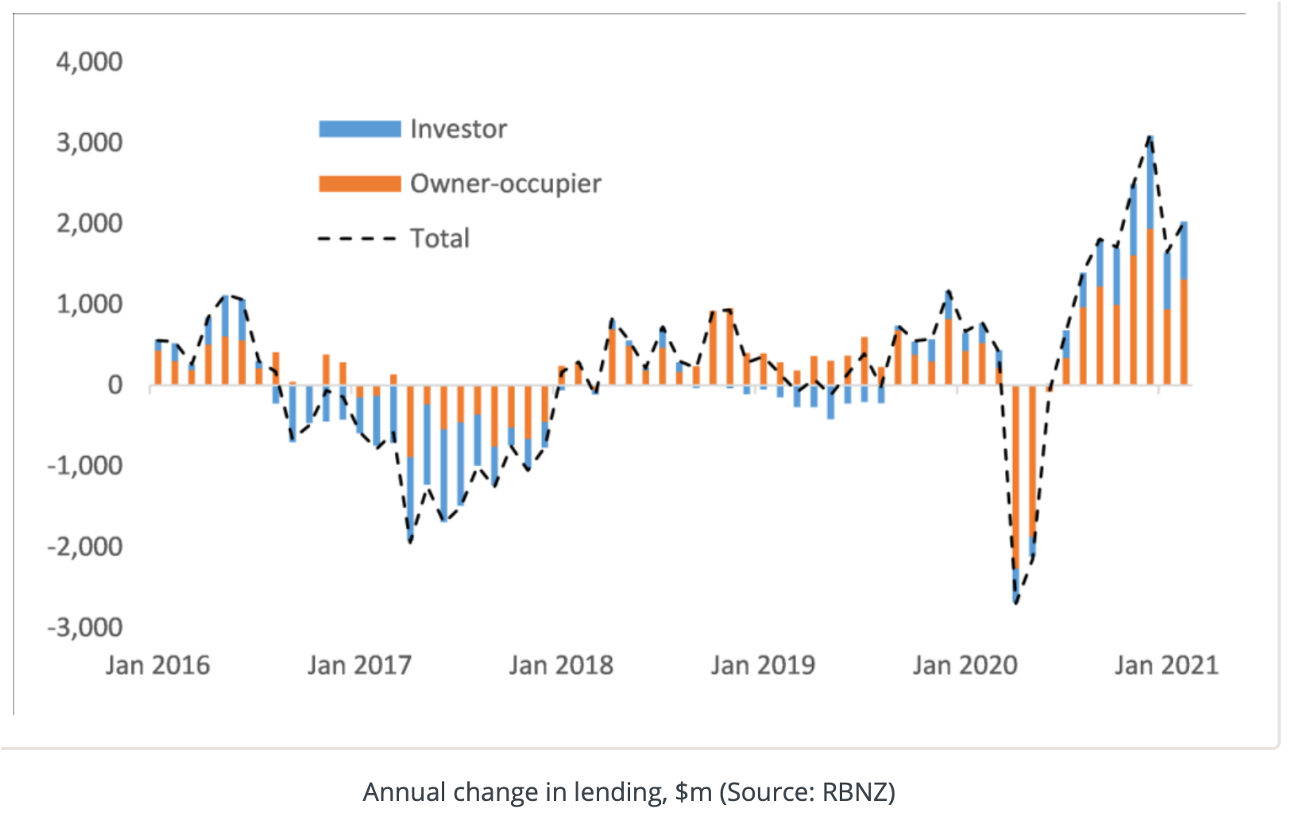

The proof lies in the counterfactual played out between May and November last year when the banks released the shackles on their high LVR lending, particularly to investors. That helped power an extra $1b a month of lending into the market, as this next chart shows. By November the Reserve Bank realised its mistake and re-imposed the restrictions, albeit verbally immediately, and then formally earlier this year. That has helped slow the market.

Now the Reserve Bank is looking to impose even more restrictions, including the potential for a ban on interest-only lending to investors, which makes up more than half of new lending to landlords and a third of all new lending. It may even impose a limit on high debt to income multiple lending, although the government is less keen because it would hit first home buyers hard and the Reserve Bank thinks it would be difficult to make the instrument more surgical.

The Reserve Bank will deliver its six-monthly Financial Stability Report next week and is expected to lay out more of its plans. The government has also been more active in looking to tie down the banks in recent weeks, as well as protecting the interests of taxpayers in the very unlikely event of a bank collapse.

We have been special in other ways too

That’s because New Zealand has been an outlier all this time in not having a formal government guarantee of bank deposits. The assumption, free-market-style, was that savers would do their research and take their chances of putting their money in a safe bank. The idea was the riskier banks would offer higher interest rates to compensate for the higher risk. There was no need to have a deposit insurance scheme because market discipline would force banks to be safe, and perfectly informed savers would do their analysis and impose this discipline. The system was held together by the idea of not having moral hazard and promising to let a bank fail in a crisis.

But the end result was an informal government guarantee for the big banks that was unpaid for by savers. No one seriously expected the government and Reserve Bank would just let one of the big four collapse, given New Zealand has the most concentrated banking market in the developed world.

So the government has proposed an insurance scheme for deposits of up to $100,000 that would be paid for by the banks themselves, who would in theory pass those costs on to savers. Robertson is also looking at being more interventionist in specifying what types of lending banks should do.

That’s fair enough in my view, because as we’ve seen over history, banks are special and powerful and ultimately it is always the taxpayer who has to pick up the pieces and wear the costs.

Orr and Robertson are also aware just how much more lending the banks could do to pump up house prices even further if they were not restricted. The May to November splurge was just a taster.

How debt could easily double

New Zealand home owners are currently spending less than 6% of their disposable income on the $300b of mortgages against over $1.5t of property. A doubling of mortgage debt would mean the collective LVR for home-owners would be just 40% and the servicing costs would be less than 12% at current interest rates, which is less than the 14% seen back in 2007 and 2008.

Home owners could easily afford it and banks could allow it. Currently, the banks assume interest rates will bounce back to at least 6.0-6.5% when they lend to a home buyer. Any lowering of that serviceability threshold to account for the much-lower-for-much-longer state of interest rates would unleash a torrent of new loans. Just imagine what another $300b of debt would do to house prices. A $1m median house price in Wellington would easily jump to $2m.

So it’s a good thing the Reserve Bank and the government are strengthening the guard rails around the banks’ involvement in the housing market and speed-limiting their mortgage machines.

Our banks are Ferraris disguised as Toyotas. Allowed a free run on a big motorway with an ambitious driver, they could move very quickly, and crash very badly.